Casey Mulligan has a response on his blog to a recent Bloomberg View column of mine about wages and the "Great Vacation" hypothesis. In that column, I basically just said that flat real wages are a puzzle for explanations of the post-2009 stagnation that rely on government paying people not to work (the "Great Vacation" idea). Casey doesn't like this. Let's go through his points...

Naturally, a supply-demand decomposition exercise is enhanced by looking at both the quantity and price of labor, also known as the wage rate. That's why my book on the recession starts off with various indicators of wage rates and their dynamics (see chapter 2 beginning on page 9).Well then I guess my article was not exactly news to Casey.

Three or four decades of labor economics research are of great assistance in this exercise.Well, I guess they've got to be good for something.

I kid, I kid!

[A] reduction in labor supply could be associated with reduced cash earnings even while it was increasing employer costs:

1. A reduction in labor supply could reduce the quality of labor, with workers putting in less effort, or doing less to maintain their skills, or become less attached to the labor market. This tends to reduce cash earnings per hour because each hour is less productive. These have been major factors in the analysis of women's wages, where most economist believe that women's hourly earnings increased as a consequence of supplying more (see Becker 1985, Goldin and Katz 2002, Mulligan and Rubinstein 2008, and many others). See also some of the literature on unemployment insurance such as Ljungqvist and Sargent's paper on European unemployment.True, but don't things like unemployment benefits and Social Security Disability only go to the unemployed? Slacking off at your job does not result in the government mailing you a check. Why would a rise in welfare-type benefits cause people to slack more? Are they sitting there at their desks feeling depressed, thinking "Dang, I could be earning almost this much if I quit my job"? I guess it's possible, but unlikely, especially given the decreased rate of quits in recessions.

A reduction in labor supply or demand could increase the average quality of labor through a composition bias. See p. 17ff of my book and the references cited therein.Wouldn't this tend to increase wages, or am I being dense? Do I have to go to p. 17ff?

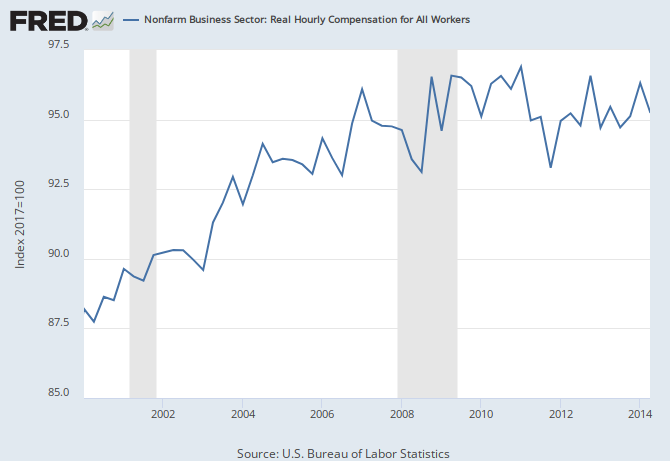

Because of fringe benefits, cash hourly earnings are not the same as employer cost. As employer health insurance expenditure has been growing over time, the growth of cash hourly earnings has substantially under-estimated the growth of employer cost.OK, but did these non-cash benefits start to increase more in the years following 2009? Nope. They flattened out just like wages. So the point I made in my article applies to this kind of compensation as well.

Labor economists have also long studied the incidence of supply and demand impulses: that is, the effects of supply and demand factors on both wage rates and the quantity of labor. The consensus is that: (a) labor demand is more wage elastic than labor supply and (b) labor demand is even more wage elastic in the long run than it is in the short run.

Suppose that the reduction in the quantity of labor were 50% due to demand factors and 50% due to supply factors, and that we had overcome all of the measurement issues cited above. Result (a) means that wages would fall in the short run, because supply shifts translate more into labor quantity than into wage rates while, in comparison, demand shifts translate more into wage rates than labor quantity. In this example, it would be wrong to conclude from reduced wage rates than supply is less important than demand for explaining the change in the quantity of labor.

To put it another way, if we found that wage rates (properly measured) were constant, but didn't know the relative contribution of demand and supply factors to the quantity change, result (a) tells us that the majority of the labor quantity change was due to supply factors. With a labor supply elasticity of 0.5 and labor demand elasticity of -3 (reasonably conservative short run estimates), the constant wage rate result means that 86 percent of the quantity change was due to supply factors and only 14 percent due to demand factors. In the long run, labor demand is even more wage elastic, and the share attributable to labor supply is even closer to 100%.

To put it yet another way, if it were true that labor demand explained the majority of the change in labor quantity, then employer costs (properly measured) would have fallen dramatically.I think it's very important to correct for the trend here. Real wages have been flat since the crisis and recession, it's true, but were growing strongly before that. Also, continued productivity growth since the recession seems to indicate that real wages have fallen substantially relative to the long-term trend.

{kind=link}

As for the inelasticity of labor supply, it had always been my understanding that the macro evidence showed a fairly high elasticity of labor supply. You'd certainly expect Mulligan, whose theory of unemployment is based on a rise in implicit taxes arising from benefit phase-outs, to take this view. Without looking at his parametrization, I can't tell if the "inelastic labor supply" story is numerically consistent with the "benefit phase-outs caused the stagnation" story, but the two stories do seem to be somewhat at odds. In other words, if you think unemployment is due mainly to people being paid not to work, then it seems like you have to think that people's work decisions respond a lot to how much you pay them.

As for the long run, the period we're talking about is something like 2009-2012, so it doesn't seem that long to me.

In other words, the flattening of wages since the recession still seems like a puzzle for these theories. And I didn't even mention sticky real or nominal wages...

(Note: I was a little unfair in lumping Mitman's theory in with the "supply shock" stories, because his model uses search frictions to make unemployment insurance reduce labor demand. I still think his model is probably pretty wrong, though!)

" As employer health insurance expenditure has been growing over time, the growth of cash hourly earnings has substantially under-estimated the growth of employer cost."

ReplyDeleteSo how many fringe benefits were the people at the bottom of the wage distribution enjoying?

Mulligan's writing and theories are really hard to folllow, in a way almost like he's trying to set up something that's not falsifiable. Is that the point? Throw a bunch of confusing stuff out there and tack on "And therefore, cut benefits for my plutocratic masters' benefit!" and hope the argument from authority convinces enough folks?

ReplyDeleteMDZX

I'm pretty sure his prediction that Unemployment cuts in North Carolina would cause all those voluntarily unemployed loafers to roll their sleeves up was both falsifiable and later proven false.

DeleteAdvocating kick-em-while-they're-down policies without adhering to an elevated standard of proof, especially in the current environment, literally makes Mulligan a bad person. If Mulligan happens to read this, please go fuck yourself.

You, sir or madam, win the internet today.

DeleteBut doesn't the stagnate wages and unemployment cause a problem to all macro theory(or at least all search and matching). Since in these models unemployment is created because of the wage being too high according to the productivity of the worker.

ReplyDeleteYeah people like Eichenbaum and Christiano use lower TFP to try explain the slow recory, that will also help Mulligan

DeleteI read things like this (Mulligan, not you Noah) and it really makes me contemptuous of the entire economic discipline. It seems to lack a lot of analytical rigor.

ReplyDeleteI'm talking about this passage in particular:

" A reduction in labor supply could reduce the quality of labor, with workers putting in less effort, or doing less to maintain their skills, or become less attached to the labor market. This tends to reduce cash earnings per hour because each hour is less productive. These have been major factors in the analysis of women's wages, where most economist believe that women's hourly earnings increased as a consequence of supplying more"

1. The women's wages example is of the opposite phenomenon. Isn't it a tad naive to assume the incentives and dynamics of people working more aren't merely the mirror opposite of the incentives/dynamics of people working less?

2. Cash earnings per hour reduced because of lower productivity is...again naive. Workers can easily be paid less for more productivity or paid the same for more productivity if the market lacks an equilibrium--greater labor supply, or weaker labor demand, allows employers to pressure current workers to work harder. Greater productivity can lower worker demand, in turn causing downward pressure on wages. A lot of things can happen, actually. The world is messy.

My problem isn't that Mulligan is approaching this issue with the sophistication of a child. My greater problem is that this naive perspective is taken seriously. In other fields this conclusion-leaping would get a grad student laughed out of the conference room. Is it me?

A bit unrelated, perhaps, but what do you think of pseudoerasmus's economic blog at pseudoerasmus.com? It's an excellent blog that combines economics with HBD.

ReplyDeleteYou are sure that economics, HBD, and excellence aren't one of those things like "fast, cheap, and good" or "consistency, availability, and partition-tolerance" where you can only ever have two out of the three?

DeleteI think the three or four decades of research may be more an obstacle to his understanding than a help because he is considering this from the standpoint of normal equilibrium times and not recessionary ones. By (a) he is saying demand can never be important unless wages are falling dramatically and recessions are always great vacations.

ReplyDeleteBrad Delong "trolls" you Noah...

ReplyDeletehttp://equitablegrowth.org/2014/09/07/anybody-surprised-job-shortage-continues-long-troll-noah-smith-lazy-monday-morning-featured-september-8-2014/

And I think he nails you on your tendency to "keep an open mind" too long. His counterfactual is hard to dispute. I am sure you are familiar with it, sooo me, having an open mind, would be interested to know why you don't give his point the creedence it seems to me it demands ?

DeLong:

Delete"I, by contrast, think that we do understand very well why it is that stagnations continue once the economy has gotten wedged.

Right now people in the aggregate are happy spending more or less their incomes, and individual managers think that if they hired more people and produced more stuff they would be unable to sell it at a good enough price to increase their profits. You might think that since there are a lot of unemployed workers they would offer to take the place of employee workers at lower wages, and after that replacement took place the profit-and-loss calculus would be different and so firms would hire more people and produce more stuff, but the labor market does not work that way. You might think that, since there are a lot of unemployed workers and no threat of inflation, central banks would lower interest rates and that would give an incentive for businesses to start spending more than their incomes by boosting investment in new capital and that would start a virtuous cycle going.

Indeed, that is the way a stagnation usually gets fixed.

But right now central banks have lowered short-term interest rates as far as they can go: they cannot lower them any further to boost spending. And so far central banks have proved unable or unwilling to promise to keep interest rates low enough for long enough to materially alter the investment spending calculus. Governments have proven unwilling to take up the slack with their own spending. And raising financing for residential construction or small and medium enterprise expansion remains very difficult because of the clogged credit channel.

So where is the mystery? What don’t you understand?

The mystery is, rather, that there are people who expect a stagnation at the zero interest rate lower bound with fiscal policy dominated by austerity and 8 clogged credit channel to be short…"

Not really a mystery. They're paid to be stupid and there's peer pressure.

"Why would a rise in welfare-type benefits cause people to slack more? Are they sitting there at their desks feeling depressed, thinking "Dang, I could be earning almost this much if I quit my job"? I guess it's possible, but unlikely, especially given the decreased rate of quits in recessions."

ReplyDeleteSo you believe it's unlikely that people might choose receiving welfare instead of working for some marginally higher wage?

My God, man! Think about it....

Welfare benefits can absolutely affect worker productivity. It isn't as important economic force as conservatives claim especially if the welfare benefits aren't big enough and it isn't as unimportant and small economic force (who practically see it as non existing or don't give a fuck and think it is always worth it) as left wingers who self identify as liberals think, especially if the welfare benefits are large enough.

ReplyDeleteThat means that you ought to try to not have too large welfare benefits from at least this perspective. It is something to consider and not completely dismiss.

The beauty of the American yes we can, strong legal system is that oligarchs need not be armed or have hired thugs for protection....well a weak legal system does the same for the pauper in welfare state ....well instead of welfare we can. yes we can put future inheritors of earth... it's a good life for the millionaires and some multi-billionaires under the law, but you need to protect this people from the welfare state people or welfare untermensch a completely different kind of army for hire is needed: the tens-of-thousands-strong army of policial and prisional militia and some thousands of wealth-protection paper-pushers.

DeleteThis is a group of people, moderately pauper or some sub or underwealthy at best with leisure time und so weiter, whose jobs are dedicated to protect and serve the oligarchy ...chi? chi-chi...

The way to think about his position is if people in net decide they need to save more, this is a supply problem because what the unemployed were producing wasn't attractive enough to prevent this and they didn't lower their wages and prices enough to discourage them and only lower wages can lower demand. The implicit assumption is monetary policy fully adjusts any changes in money demand.

ReplyDeleteToo much words, too much empty information...

ReplyDeleteThe fact that this debate between two economists can be conducted in this way is proof that economics is a disaster.

ReplyDeleteWhat are the truth conditions for Mulligan's claims? For Noah's? There are none, either way! It's Sudoku all the way down!