"Past performance is no guarantee of future results." This is the most common caveat in finance. It means that, despite the fact that past and future are often correlated, that correlation is no guarantee; something may happen in the future that never happened in the past. In technical terms, economic and financial processes might not be ergodic.

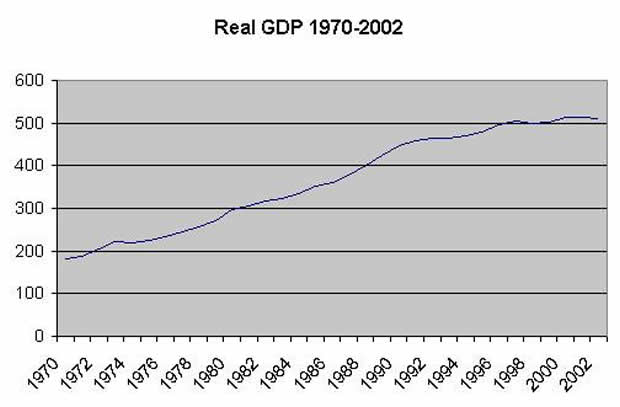

This is why, unlike Mark Thoma, I am not reassured by a long-term plot of United States gross domestic product. Dr. Thoma writes:

As you can see from this picture, historically we've always recovered from recessions. Eventually. ... I am confident that we'll return to trend this time as well, the question is how long it will take us to get there.

He illustrates this with the following famous graph:

The idea is that because this graph sort of looks like a straight line (although if you look closely, you'll see that it's not!), that it will continue to look sort of like a straight line into the future.

But off the top of my head, I can think of no good reason to think that this is true. The kinda-sorta stability of the long-term U.S. GDP growth rate is not a law of the Universe, like conservation of momentum, which is (we hope) fixed and immutable. It is a past statistical regularity whose underlying processes we don't fully understand. There may be solid, long-term factors that will keep our growth at this "trend," or there may not.

Here, check out a long-term graph of Japan's GDP, in levels:

Looks a bit different, eh? If you looked at this graph in 1996, you would expect Japan to return fairly rapidly to the exponential growth "trend" it had enjoyed up until 1995. Instead, Japan's GDP has remained flat in since then (this is also true in real terms). Here's a picture of Japan's real GDP growth rate over time:

{kind=link}

Japan's growth history looks very different from ours. It seems to have suffered some "trend breaks" in growth. And my question is: Why should we believe that this will not happen to us?

One common answer is that long-term growth for a mature economy will continue at roughly the rate of technological progress. But this is a tautology, since economists measure "technological progress" simply as the the long-term rate of GDP growth. This leads some economists to look at slowing growth and conclude that technological progress is slowing. And maybe they're right! The point is that whether long-term growth represents "technology" or some combination of underlying processes, there is no law of the universe that says that these processes grow at a constant exponential rate.

And in addition to "trend breaks," there is no guarantee that U.S. GDP does not also contain unit roots. In other words, the assumption that the dip in U.S. output that we call the "Great Recession" will be made up for by fast growth in the future is unfounded. Even if the U.S. returns to its "trend" growth rate of 2 or 3 percent, there seems to me to be no good reason to believe that it will return to its trend level.

Update: I don't want to mislead with the Japan graphs. In per capita terms, the growth slowdown since the mid-90s is much less pronounced. And before the 70s, Japan was well below the richest industrialized nations in per capita GDP, so its mid-70s slowdown is to be expected. But my point about Japan was that the U.S. long-term GDP plot, which is so often used to predict a return to 2-3% growth, is not particularly universal.

Update 2: What "policy choices," you may ask? Well, the answer is that I don't know. My instinct says that clinging to an increasingly broken health care system can't be good for long-term growth. The first-ever U.S. debt default, which Republicans look ever more eager to flirt with, might end our special place in the global economy. Accepting a permanently lower level of taxation and spending might starve the nation of infrastructure and R&D, thus reducing our trend growth. Just some thoughts.

Update 3: I see that G.I. over at The Economist has said much the same thing. And wow...the drops in output in Sweden and South Korea following those countries' financial crises sure look like unit-root drops to the naked eye!

Update 4: Mark Thoma writes a very long and good post about the "return to trend" controversy, which also cites other long and good posts by Brad DeLong, Greg Mankiw, and Paul Krugman. Definitely read it! And, of course, it almost goes without saying that I think we should try our best to boost output back to the "trend," whether or not that would happen on its own.

Update 5: Brad DeLong has a graph of UK GDP that also shows that "returns to trend" are not universal.

GDP is also dependent on demographics. This helps to distinguish the US from Japan.

ReplyDeleteThat's why we have GDP/Cap, Anon.

ReplyDeleteI took a hard look at U.S. GDP last fall, and concluded we are dying.

I really see no reason for optimism.

Lo siento,

JzB

It seems pretty misleading to compare a plot of log GDP over time to plots of GDP levels and growth rates.

ReplyDeleteThe ol' straight-edge on graphpaper technique does not meet your standards? You have standards?

ReplyDeleteI've never quite grasped why economics is not more covetous, say, of an analysis of the economic growth driven forward by the industrial revolution. Say, one that featured components, like conquest or fossil-fuels, as well as the black-box of technology -- maybe even break open the blackbox (what a concept!). It seems like it would come in handy, at times like this, when globalization, peak oil and climate change are issues.

Yeah I do think there has been some over optimism in the blogosphere lately. I even think you can acknowledge that someday japan may return to trend but its kind of an "in the long run we are all dead" kind of thing.

ReplyDeleteIt may be that our recession was not as deep as the Great Depression but it may wind up being as as long as the shallow fall in output has a corresponding anemic period of low growth that eventually gets us back to trend. The trend stationarity argument isn't overly reassuring.

Jason -

ReplyDeleteIf the level is flat, the log is flat, dude.

The reason the Japan graph is misleading is because it's in nominal terms, not because it's in levels.

Really great blog. My friends referred me your site. Looks like everyone knows about it. I'm going to read your other posts. Take care. Keep sharing.

ReplyDeleteAfter looking at Brad's UK chart, which I don't find convincing, I don't find your Japan chart convincing either. UK output did return to its pre-WWI trend; it just took a long time to do so, in part because there were some serious setbacks along the way. Why should I not expect the same to be true of Japan?

ReplyDeleteGranted, there is no reason to think that a nation's output should follow a single exponential trend in the first place, but if that were my theory, then the lesson of the UK data would be that we should not be discouraged by a couple of decades of failure to regain the trend, because it can take quite a bit longer. The Japan chart today looks a lot like the UK chart did in the mid-1930's. If the subsequent performance is comparable, then Japan faces a bright future.

1. Thoma and others believe that we will return to the long term trend shown in the first graph. However, looking closely (as you mention), the trend line in the graph moves to match the data as necessary, so how can we argue with that? In other words, if they are arguing that we will close the output gap relative to the pre-recession trend line, then it's only an opinion. If they are arging that the data and the trendline that is a moving average will eventually converge, then they're stating the obvious.

ReplyDelete2. Why are apparently intelligent people basing their predictions for the future of US GDP on historical precedent from periods (e.g., history back to 1870?, the post-depression/post-WWII expansion?) when the US population and economy were both expanding rapidly and we were grabbing a larger and larger share of the world's resources? We reached the top, people! To think we can continue to grow like Topsy because we did so in the past is ludicrous.

3. The most recent pre-recession GDP trend line was that of an economy on steroids (excessive credit feeding a housing bubble). Finance was juiced. Employment was juiced. Incomes were juiced. Consumption was juiced. All of these contributed to a GDP that was juiced. Those who are arguing that we will close the output gap by 2014 or 2015 probably also believe that hitters will be back to clobbering 70 home runs in a few years. Based on a relatively conservative 2% real growth rate assumption for the pre-recession trend, we still have an output gap of close to 6%. The hard reality is that real growth must AVERAGE 3% for SIX YEARS to close the gap. Are they serious, or are they so lost in univariate vs. bivariate arguments and the like that they have lost all common sense?

Technological progress - i.e., productivity improvement due to it - is not yet slowing, but it will in the next few decades if not sooner, since Moore's Law and similar rules of thumb are about to hit a wall. But what is indeed happening is the beginnings of saturation of productive capacity, and that may not be cyclical. I.e., the utility of technological progress for productivity improvements has at least temporarily disappeared, and that may be permanent if labor can't catch up.

ReplyDeleteLook at the ratio of productivity to wages over the past 30 years: productivity has improved steadily, wages have been and (and in the very recent past, declining). If that's due to technology - as I think it is - then it indicates that the economy has become too productive for consumption to be able to keep up, and it's can't keep up because wages can't keep up, and wages can't keep up because technology has been devaluing labor.

I'm not an economist - I'm a computer scientist - so I'll let you put this in economist lingo, but you're a smart guy, Noah, I think you can do that if you care to.

I might mention (as a qualification) that when Moore's Law and similar limitations on chip power consumption do hit a wall - and that is already starting to happen with power consumption, further advances will still be possible but will be more costly, since parallelism and redundancy will be the likely mechanism for it. I.e., the steadily decreasing cost of technology may not continue in the long term like it has in the past 30 years or so. Software, however, is already free to a significant extent; I expect that trend to continue (i.e., more of it will be free).

Andrew Bossie-

ReplyDeleteThe whole doom and gloom thing is a bit overkill cause really the recession we just experienced wasn't as big or as long as the Great Depression. While this has been the biggest since then doesn't mean everything's bad. Technically the recession has ended, it's just that people won't really see the effects of that for a while, like unemployment dropping and such.

And there is a positive to be seen in hitting the lowest point of the recession. The business cycle consistantly shows that following the lowest point we're going to see an upswing to get back on track and then surpass the original level we were at.