Dan Murphy is a fellow graduate student here at the University of Michigan, and will be going out on the job market next year. We were having a discussion about why the finance industry might have gotten so large in the U.S. in recent decades, and he decided to write up his thoughts on the subject, so here they are!

{kind=link}

***

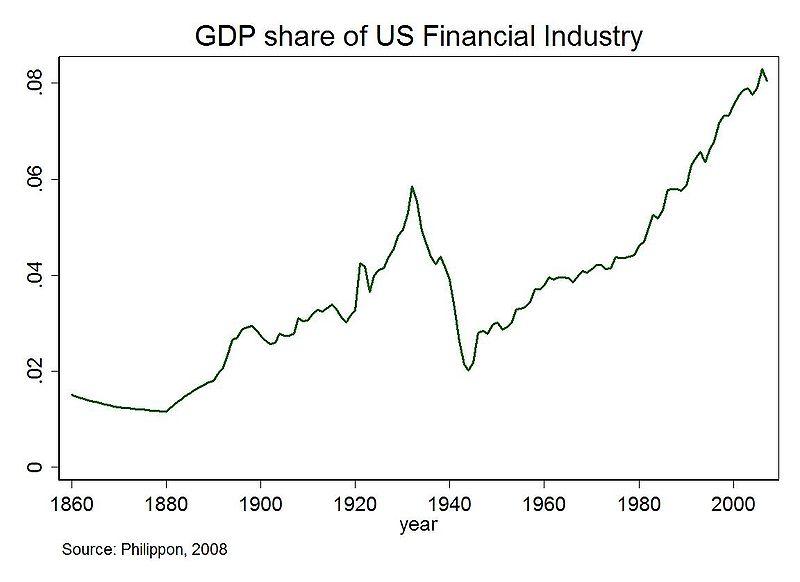

In an earlier post Noah solicited possible explanations for the increasing share of value added of the finance sector over the past half century, and especially the rapid increase in the 2000s. I thought I’d throw a few ideas into the conversation.

To understand why the share of income received by finance has increased, it is first important to discuss how finance adds value and generates income. I can think of three primary services that financial institutions provide:

1) Making Markets: Financial institutions often act as a marketplace, matching buyers with sellers. In return for this service the institutions charge a fee, and this fee is counted as their value added. This function of financial institutions can be compared to the function of a farmers’ market that provides a centralized meeting place for farmers to trade their produce. A group of people organize the market (find the location, provide tents and porta-pottys, etc), and in exchange the market organizers are paid a percentage of every transaction that takes place. The organizers have an incentive to promote trade because their income is growing in the volume of transactions. In the U.S. economy, financial institutions are the market organizers, and their income grows with the volume of transactions (GDP). For example, credit card companies facilitate our purchases, and they earn a fee every time we buy something with a credit card.

2) Managing Risk: This is really a specific subset of the first category, but it is an important enough function to warrant further discussion. Financial institutions manage counterparty risk, and in exchange they are paid a fee (often referred to as a “haircut”). More concretely, consider a wheat farmer (let’s name him Fred) who observes that the current price of a barrel of wheat is $10. At that price he is willing to plant enough seeds for X barrels of wheat. The problem for Fred is that the price of wheat may fall by the time of harvest, in which case he will wish that he hadn’t put in so much effort planting wheat. Financial institutions can solve this problem for Fred by promising to purchase wheat from him for just under $10 at the time of the harvest. Fred is willing to accept the slightly lower price in exchange for price certainty.

Meanwhile, consider a baker (let’s name him Ben) who purchases wheat to bake bread. He can sell a loaf of bread for $5, and his profits from the sale depend on how much he must pay for the wheat. Ben is happy when the price of wheat falls, and he very unhappy when its price increases. Therefore he is willing to pay a small fee to guarantee that he will be able to purchase wheat for around $10 a barrel for the next year. Financial institutions help Ben by promising to sell him a barrel of wheat after a given amount of time for just over $10. In doing so, they offset their risk exposure to their contract with Fred through their contract with Ben, and in the process they earn a fee.

3) Investment Intermediaries: Financial institutions manage investments for clients and offer advice (on investing, planning for retirement, etc). Many savers are willing to pay for these services because they a) believe that financiers have expertise that will earn them a higher return on their savings, and b) because they need an intermediary to help them purchase assets (if I want to buy gold (I don’t), presumably I’d ask a financial institution for help rather than walking around with cash and a wheelbarrow).

Borrowers pay financial institutions to help match them with willing lenders. Often this takes the form of duration transformation, in which finance companies borrow from short-term savers to lend to borrowers over a long time horizon. For example, financial institutions help cities issue long-term municipal bonds to pay for roads and schools.

Now that we’ve laid out some of the basic functions of the finance industry, let’s see if we can find a reason that its value added should increase so drastically.

Making Markets: Based on our example above, it appears that the value added of making a market is in “greasing the wheels” of trade in goods and services. If this is true the value added of financial institutions should grow in proportion to the growth of output (trade), holding constant the cost of greasing the wheels. Of course the costs of facilitating trade have likely decreased over the past half decade. Consider credit cards: You may purchase the same amount of groceries as you did twenty years ago, but since your now use a debit card instead of a check, the cost to your bank of facilitating that purchase is much lower. Could such cost-cutting increase the profit share of the finance industry? If the banking services industry is noncompetitive, then perhaps, but even in this case it’s difficult to explain such a drastic increase, especially between 2000 and 2007.

Managing Risk: One reason that the value of risk management could grow more than the aggregate value in the economy is that as the economy grows, there is more risk to hedge. For example, as aggregate income grows, consumers want to insure against more events in their lives (life insurance, for example). Our ancient ancestors’ income was so low that it was all spent on food. Since all adults spent their time hunting and gathering just enough to feed their own families, there were no “financiers” available to help people insure against a wolf killing the head of the household. Contemporary Americans can produce food at much lower cost, and thus we can devote labor resources to managing insurance contracts. But people have been able to insure against a range of events in their lives (floods, fires, death, etc) for decades, so I can’t imagine that an increase in demand for life insurance can fully account for the increase in the value of the finance industry. It is true that firm-level risk has increased through the 80s and 90s (Diego Comin has done extensive research on this topic), and this increase in risk could correspond to higher demand for insurance. But again, the acceleration in finance’s value added share in 2000 did not correspond to acceleration in idiosyncratic risk.

Investment Intermediaries: Here I think is our answer for the rapid increase in the observed value added of the finance industry around 2000. My guess is that the average person believes that financiers have superior knowledge of investing, and that this superior knowledge will earn them higher returns on their savings. There are two primary effects that increase the computed share of value added attributed to the finance industry: Fist, when returns are high, as had been the case in housing and stock markets until the recession, retail investors (and even pension funds) are less concerned about the fees they pay to fund managers (my wife didn’t know she paid fees, she just sees how much money is in her account, and if it’s more than the last time she looked, she’s happy. I hear that some pension funds operate under similar rules of thumb). If I give you $10, and you return me $20, I’m not overly concerned with the fact that you could have returned me $25 but instead kept $5 for yourself. You tell me that you are special, and that you earned it, and I am happy enough that I just doubled my net worth that I don’t think twice, especially when other supposedly talented fund managers are also charging high fees. This effect will be exacerbated when cash and bonds offer low returns while other assets (stocks, housing) offer sky-high returns because investors are even more likely to believe that the fund managers were special enough to earn higher returns than those offered by the savings account at the local credit union.

Note that this explanation does not require that we specify why returns for some assets are higher than others. But I will simply suggest that if investors seek high yields by investing with managers who hold an appreciating asset (perhaps housing), that behavior could contribute to a price bubble and increase the share of value added attributed to the finance industry. Interestingly, finance’s share of value added grew disproportionately along with the price of housing leading up to the recession in 2008 and fell during the recession.

Of course the high fees paid to financial intermediaries raise the following question: Why has competition among financiers not prevented high fees from increasing their share of the returns to asset price appreciation? In other words, if you reap a massive profit by charging me $5 to manage my money, why does someone else not offer to charge me $4? One reason may be that you are Goldman Sachs, and you have established a reputation that you are worth the $5 (regardless of whether this is true). Since I don’t know the “true” value that your service adds, I simply assume that you are worth the $5.

Similar phenomena occur in other markets. For example, I bought basketball shoes last week, and because I haven’t bought shoes in ages I have no idea which brand is the highest quality. Nikes were $30 more expensive than what appeared to be a similar shoe from another brand. Since Nike has established in my feeble mind a reputation for making quality basketball shoes (through advertising perhaps), I forked over the extra $30.

I have not had the opportunity to purchase services from Goldman Sachs (my piddly graduate student stipend essentially becomes cash temporarily stored under my mattress). But I imagine that if I did have reason to do so, especially before the financial crisis, I might be willing to pay their exorbitant fees, especially if they are selling the opportunity to make money. If Nike sells me the chance to dunk, I will gladly buy even if some Nike employee gets to dunk ten times as much. Likewise, if Goldman sells me the opportunity to make more money at the cost of some money, I will buy even if doing so allows them to makes lots of money as well.

So yes, I do believe that some of the rising value of the finance industry is in its ability to efficiently facilitate trade and manage risk. But another reason, which I would attribute to the acceleration in the growth of finance’s value added and profit shares around 2000, is likely due to the financiers’ ability to sell their services, an ability that grows in strength when certain assets are appreciating because investors are willing to pay to hold appreciating assets. If this appreciation is due to technological improvements, as in the 90s, then investors are, over time, benefiting from the financial services, even if at a high price. But if the appreciation is due to a bubble, or to expected economic growth that does not materialize, then the incomes in the finance industry will increase without a corresponding increase in aggregate income, translating into a rapid rise in the finance industry’s observed share of value added.

I think that you need to look at this in the historical terms of the rise of the rentier economy, which sequentially lead to the decline of the Spanish, Dutch and English financial empires. Essentially, there is a pattern of trade/technology advantage, followed by the growth of a middle class, followed by wealth following investments in government debt and creation of rent opportunities, followed by decline. For more discussion, please see 'Economics: Repeating Rhymes' at http://somewhatlogically.com/?p=562

ReplyDeleteEssentially, all the countries mentioned failed to invest in their own development and industry, for example, "At their peak, the wealthy of Holland owned one quarter of England’s public debt, along with one third of the shares of the Bank of England and the British East India Company, while their manufacturing mostly peaked in the 1720s. Earlier, travelers had commented on the wealth of the Dutch middle class, but in 1764, English writer James Boswell noted: ”Most of their principal towns are sadly decayed, and instead of finding every mortal employed, you meet with multitudes of poor creatures who are starving in idleness.”

Also, the rise of the financial sector pay and services have very little to do with benefit to the economy, and much to do with government policy, as discussed by Bartels, as quoted here. "Projecting Inequality' at http://somewhatlogically.com/?p=254

It could well be argued that the two Roosevelt administrations drew us back from the edge of the self-inflicted collapse. Why should one invest in a company that has all those messy employees, supply issues, market concerns etc. when if you're rich enough to be invited to join Madoff's funds, you can get 25% annual return. Crowding out by the financial sector, anybody?

JRHulls

Somewhatlogically.com

Nice summary!

ReplyDeleteHowever, it should be quantifiable how profits booked at the time trades were made compare to any losses incurred in the trade over its lifetime. I believe Andrew Haldane has some estimates and the losses dwarf any growth in value-added. Therefore, I am a bit surprised you don't give this kind of incentivized time mismatch more prominence in your analysis.

By all three of your criteria, the finance industry is an epic fail for society.

ReplyDelete1) As market maker, you argue correctly that the finance share should not grow faster than GDP, but it has - and quite dramatically so. In fact, finance has captured an increasing share of total corporate profits.

2) Managing risk. Yes, they managed to socialize all the risk and privatize all the return. That is value subtracting.

3) Investment intermediaries. If there were real value here for the alleged services rendered, people's net worths would be rising. The opposite is the case, and financial intermediation via bundling and tranching into derivatives which no one can rationally price or evaluate is a big part of the reason why. As intermediaries, they have reaped enormous profits while impoverishing most of the rest of the population.

The real answer is that through lack of regulation they have found ways to extract rents from society, and have given close to nothing back in return. The golden age of the post WW II era corresponded to a finance sector whose share of total corp profits was under 30%. Now it's around 50%.

Money and power are fungible, and this leads to a spiral of increasing wealth accumulation at the top. The whole thing is, in Krugman's words, a giant scam.

And it has been dragging us down for longer than your life time.

Cheers!

JzB

Here's some econ 101 analysis. (Well, from my version of econ 101!)

DeleteMarket making is a natural monopoly -- easier and more efficient if only one firm is doing it.

Private monopolies generally extract monopoly profits if they are allowed to.

We can see that this is how the VISA/Mastercard duopoly makes bundles of money. Through monopoly power.

The classic solution is for all natural monopolies to be provided as public services by the government.

In past years many market makers were effectively run as not-for-profits (VISA when it was owned by a bank consortium, NASDAQ when owned by a consortium of dealers), and they've since been converted to for-profits.

Also, many (credit cards) were not monopolies yet, and the natural process of mergers to make them into monopolies had not yet occurred.

Once they became for-profit monopolies, the increased share of profit extraction was natural and predictable.

Drat. This hypothesis seems to fail the "1920s test", given below -- it doesn't work for the 1920s as far as I can tell.

DeleteWould you be able to test your "JUST GIVE ME THE MONEY!" hypothesis?

ReplyDeleteIf the growth of finance's share of GDP is linked to returns, would the 2nd derivative of finance's share move in tandem with the size of returns.

Bigger returns (i.e Bubble time) = Acceleration in finances share of GDP?

Or something like that. Finance may follow a trend that has a negative second derivative (concave), but then you you would expect the deviation from trend growth to move with returns?

Here's Haldane.

ReplyDeleteJzB

Are 2 and 3 related? I mean there are risks we insure against now that our ancestors didn't. For example, we insure against the risk of outliving our ability to work by retirement savings, which in turn go through financial intermediaries. Maybe a lot of saving/investing is some form of risk management (eg against job loss) that previously people did not do (or could not afford).

ReplyDeleteLike, most of that has been around for a couple of generations. IIRC, the massive changes in the financial sector apply to the last thirty years (I.e., after we tore down the New Deal structures, and found out why they were there).

DeleteLiquidity and market risk are also important parts of #2, not just counterparty risk.

ReplyDeleteAlso, you forgot financial innovation. There are many markets (like commodities markets, electricity, renewable energy credits, i could name dozens), that have seen extremely rapid financial innovation in the last 10 years. This has led to the rapid growth in the need for #2 and #1.

Also, #5: Accounting and regulatory rules have become ever more complex. BASEL MCMXLVII, or whatever we are up to now, plus OCC regs, is a full time job and now we have models just for regulatory purposes.

Financial innovation is a part of making markets (#1), and its value is derived from the value of the trade in goods and services that it facilitates. Financial innovation increases the value of the finance industry, but it does not by necessity increase the finance industry's share of value added.

ReplyDeleteI wonder about financial innovation.

DeleteWhat is it, exactly? To me it seems a definition of degrees.

Is a composition of existing financial products financial innovation (i.e. a CDO)? I would argue that it is only if it produces results for the buyer that the sum of the components cannot produce outside of the new vehicle at a reasonable cost.

Computer technology differs just this way. A billion transistors is not the same thing as a CPU. The CPU's architecture makes the product's function fundamentally different from that of its components. Hence I call it innovation.

The computer engineer's value-added is that he extracted from a billion transistors functionality that they do not have as stand-alone components.

Now, we know that some composite financial products produce new functionality through regulatory arbitrage, whereas some produce it through imperfect correlations, for lack of a better description.

So we could argue that they do behave like technological innovations.

But what if some of these innovations work by creating information asymmetries and thus help sellers sell lemons at higher prices than they would in a less sophisticated, more transparent market?

If, in other words, an innovation operates not by producing fundamentally unique and new functionality, which in turn produces value-added, but instead acts as a means to redistribute wealth from buyers to sellers, could it be that parts of the so-called value-added from "financial innovation" are redistributions in disguise?

Good summary, but I think it misses something about financial asset wealth vs tangible asset wealth.

ReplyDeleteWhile housing is tangible, "mortgage backed securities", and CDS/ CDO "financial products" (Credit Default Swaps & Obligations) are not.

As more wealth is "financialized", the finance industry gets bigger.

Similarly, bonds today are a financial product. It makes sense that an economy with $100 trill in total bonds has a much larger financial sector than one with $50 T -- and what is the limit to financial institutions in creating bonds/ obligations?

There were too many AAA rated financial products in the pre-Great Recession housing bubble. There should be a limit, perhaps GDP for a year (or two?), on the total amount of AAA rated bonds available -- and once that limit is reached, new AAA bonds would require lower ratings on the worst older bonds.

Finally, gov't debt has to be handled by the Finance Industry. Voter desires for "free money" benefits from the gov't, resulting in gov't over-spending, require the gov't to borrow. As gov't borrowing goes up, there will be more GDP in Finance.

Perhaps we can answer the question by simultaneously asking "why did the financial sector's value-added share rise so sharply in the 1920s and 1880s?"

ReplyDeleteThe same reasons or different? If the same, then perhaps we've discovered something systematic. If different, then we ought to figure out why the reasons differ.

Also, rather than asking, "why did the value-added share increase" in total, should we not worry more about deviations from trend growth in relative size?

I.e. why did we see abnormal growth in the financial sector's relative size (assuming that normal growth is something that more or less tracks the deepening complexity of a modern economy)?

"Perhaps we can answer the question by simultaneously asking "why did the financial sector's value-added share rise so sharply in the 1920s....."

DeleteYes , and then why did it decline so much in the 1930's and after , and then why were the post-war decades such a period of both financial stability and unparalleled , and widely-shared prosperity ?

What common features did the 1920's have with the past few decades that required a large financial sector with an obscene compensation structure , that distinguished those two periods from the one lasting from WWII to the 1970s , with no such requirements ?

It's very curious , but of no practical importance , I'm sure . It might be a good topic for some future economic historian with time to waste.

I think it may be of practical importance because we need questions like those to identify the necessary conditions of an outcome and to weed out unnecessary or even confounding variables.

DeleteI don't know how to phrase it exactly, but my raw (and maybe inaccurate) intuition says something like this:

1. Consider a set of statements S.

2. Consider a set of observable phenomena P', which can be described by a set of statements S' together with some logical operators.

In this case P' is a set of observable outcomes associated with a generic financial sector expansion- a financial sector expansion that may occur at any time, regardless of any outside factors, as long as the conditions described by S' exist.

3. S' is a component of S.

4. Now consider observable phenomena P'' and P''' that can be described by sets of statements S'' and S''' where S'' and S''' are both in S and S'' U S' and S''' U S' are non-empty.

I think of P' as the "core" of the phenomenon of an expanding financial sector: those phenomena which are always manifest when the financial sector expands.

To arrive at S' and therefore describe these universal, necessary features in the most refined way possible, we have to somehow filter S into S'.

The danger arises when S' is, for example, inside S''', which fully contains S'' such that there is at least one statement x that is in S''' but not S''. In such a case, we may arrive at S''' and suspect that it is S'. This would happen if we only observe P'''.

Empirically, our theory that the logical synthesis of the statements in S''' correspond to observations manifest in P''' will not be falsified, but our theory will also not be as refined as it can be- it will include statements we do not need to describe the necessary (or fundamental) reasons for a financial sector expansion.

But if we describe S'' as well (i.e. the 2000 period AND the 1920s) we would notice that there are statement x which are not in S''' and we would therefore be able to refine "a little closer" to S'.

If we do this several times and as long as each time we write down sets of statements that produce testable hypotheses with each new set of statements of cardinality lower than that of the smallest set of statements we previously used, we will make progress towards S'.

Something like that.

If we apply the "1920s test" and ask what the common feature was, the answer which pops up is rampant fraud, and government tolerance of that.

Delete“But again, the acceleration in finance’s value added share in 2000 did not correspond to acceleration in idiosyncratic risk.”

ReplyDelete???

The amount of risk that the financial sector transferred from the rest of the economy into their own (or the taxpayers) balance sheets increased a lot over the period.

“So yes, I do believe that some of the rising value of the finance industry is in its ability to efficiently facilitate trade and manage risk.”

You got to be kidding. Give me one example. As far as I know it is still all value at risk models - and I hope that you are not referring to the credit rating institutes.

PS: two real factors might be that trade has increased much faster than the general output, and that the level of debt has gone up (i.e. creating more volume to earn money on).

DeleteAlso, with respect to the level of competition – in addition to the problem of establishing a reputation (I know of people with their own funds who outperformed the big competitors for years in a row but still live on noodles due to not being able to attract large enough amounts of capital yet) there are generally really high barriers for entry into the financial sector.

Well thought out. IMHO the following are roughly the way things happened:

ReplyDelete(1) The global savings glut requires an increasing "effort" (read compensation and personnel) devoted to scouring out better returns to the capital holders, who are, precisely because of that distinction, not particularly industrious (the median capital owner, that is. This is my conjecture and always has been: basically industriousness does not typically spring from the progeny of multimillionaires but from the lower economic classes).

(2) Growing income disparity has caused a global concentration in the hands of very few. This led to crafting of global legislation and regulations that perpetuated and extended the search for higher yields on capital, leading to instruments that allowed incredible leverage on base returns. It also necessarily led to imprudent lending in many portions of the global economy, most prominently in the U.S. housing market.

(3) Then came the Minsky Moment

(4) Economies will probably continue to swing the same way like a pendulum going forward, unless they (starting with the U.S and Europe), are essentially run by hard countercyclical computer algorithms, on policies, both economic and regulatory :-)

Looking back, it is likely that a lot of the profit (and value added) reported by the financial sector in the run up to crash was simply an accounting "error" - the values, the profits and the value added were never real.

ReplyDeleteWith advancing technology, and a glut of savings, the margins and profits available to the financial sector as a whole should be declining.