Paul Krugman raises a puzzle:

[C]orporations are taking a much bigger slice of total income — and are showing little inclination either to redistribute that slice back to investors or to invest it in new equipment, software, etc.. Instead, they’re accumulating piles of cash.Tyler Cowen thinks there is no puzzle:

If there is a problem, it is because no one sees especially attractive investment opportunities in great quantity...That’s a problem at varying levels of corporate profits and some call it The Great Stagnation.But I'm not satisfied with this answer. If there is a Great Stagnation, and corporations see no attractive opportunities for growth, then shouldn't they just return their earnings to shareholders as dividends?

Standard corporate finance theory says that companies try to generate returns for shareholders in one of two ways. Either 1) the company reinvests its earnings in the business (i.e. "business investment"), raising the company's value and allowing shareholders to reap a capital gain, or 2) it pays its earnings to shareholders as dividends. Now, since the 1990s, we've gotten used to thinking of companies as rarely paying dividends. But the reason for that was that there were (or at least, companies thought there were) many important growth opportunities to be had; companies took their earnings and reinvested them.

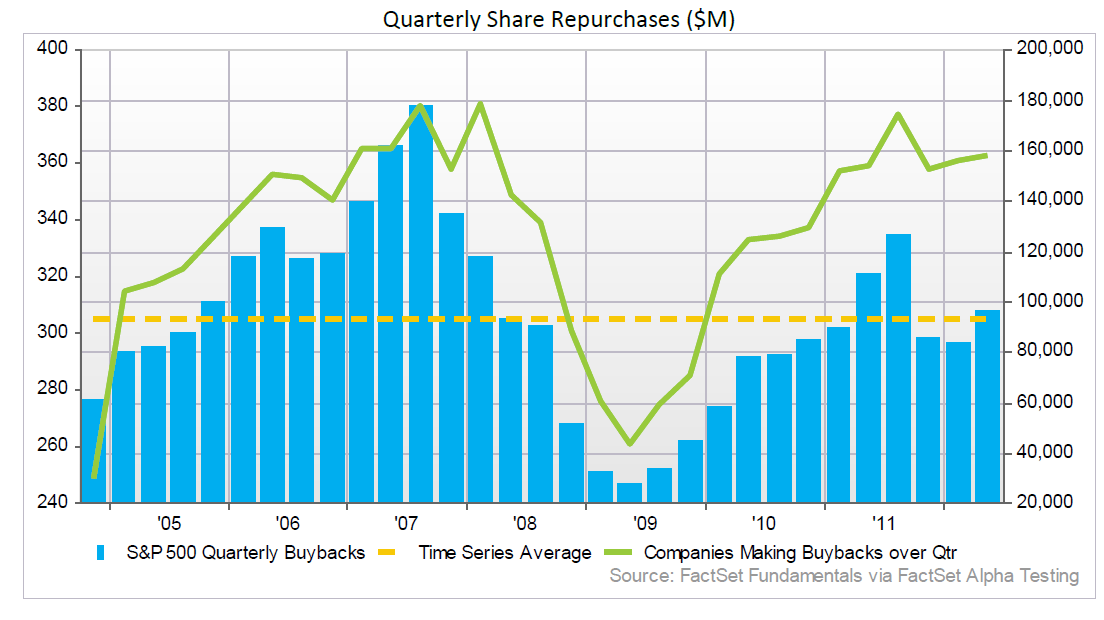

But now, U.S. companies are taking their earnings and holding them in short-term marketable securities ("cash"). That money is not being reinvested in the businesses. And it's not getting handed back to the shareholders as dividends; in fact, dividend payout rations and dividend yields are both at historic lows. (Share buybacks are reasonably strong, though that still doesn't explain the cash hoards, especially with interest rates so low.)

{kind=link}

{kind=link}

If companies saw a Great Stagnation coming, you'd expect them to be giving shareholders their money. But they're not. Why?

I'm not much of a corporate finance guy, so I'm not up on the literature on questions like this. But a few possible explanations could be: 1) corporations want to invest, and just haven't decided what to invest in yet. Uncertainly about the Chinese economy, the European economy, new technology, etc. means that corporations think there will be good growth opportunities but as yet have no firm idea of what those opportunities will be. 2) The link between management and shareholders has totally broken down. Management is acting in their own interests instead of shareholders', and shareholders haven't really noticed this, possibly because dividends were so low in the 1990s and 2000s. 3) Companies do intend to pay some big dividends, but they expect an imminent decrease in the dividend tax rate, so they're sitting on cash for a year or two while they wait for that. 4) Companies are holding the cash as insurance against a possible imminent calamity, such as a new financial crisis, in which they will need lots of liquidity.

Anyway, answering this puzzle is a task for corporate finance researchers. But I think that there is clearly a puzzle here. A lack of good investment opportunities, or a Great Stagnation, is not enough to explain the patterns we are seeing.

(And yes, I realize that this "puzzle" is really just the question of why corporations hold large cash balances at all. But in the current environment, with cash holdings at very high levels, it's an even more salient question than usual.)

Update: Tim Taylor flags some interesting research on the subject. It turns out that the trend toward holding more cash started in the 90s. Also, the paper Taylor cites mentions another reason for holding cash, which I forgot: repatriation tax avoidance. The tax dodge explanation rings true to me, whatever other factors are also present. This means we could induce companies to hold less cash by cutting corporate tax rates.

Speculation culture (cheap shot I know)? Investors don't hold stocks long enough to reap dividends.

ReplyDeletea quote from a Hollywood movie:

Sean Parker: You don't even know what the thing is yet. How big it can get, how far it can go. This is no time to take your chips down. A million dollars isn't cool, you know what's cool?

Eduardo Saverin: [Sarcastically] You?

Eduardo Saverin: [the scene shifts back to the deposition room] A billion dollars.

Agreed, Mr Noahlot.

ReplyDeleteBut I skeptical that there could be any quantifiable consensus even among corporate finance researchers. This is one entrenched puzzle! I can see why Cowen might sleep better ignoring it

1b) or 5) Companies, observing the recent increase in volatility, find or expect speculation to be more profitable than investment, and need liquidity for that purpose.

ReplyDelete2b) or 4b) Companies are amassing cash to buy back their own stock when next there is a sustained fall in stock prices, enriching executives and major shareholders that way. (The divergence of interest is between major shareholders and minor ones, rather than management and shareholders en bloc.)

The question that Cowen misses is why corporations think they are better at investing in bonds and bank reserves than their shareholders. And in many cases, such as Apple right now, its not clear that the shareholders agree with them, since they seem to be valuing corporate cash-on-hand at significantly less than $1-for-$1.

ReplyDeletePut me in the "fear of another calamity" camp. The chart over at the Atlantic shows in all three charts that the Cash Stash didn't start spiking upward until 2006-2007. That's conveniently the period when the subprime market began to deflate, and the recession first got its start.

ReplyDeleteHolding it in cash means they have guaranteed funds at hand in case growth drops down again, and they have to run in the red for a while.

If it weren't for the charts, I'd suspect that companies were holding higher volumes of cash because the business environment is so competitive and quickly changing.Companies might suddenly find themselves deep in the red, and if they don't have a cash supply to keep operating until they can make decisions to adjust or shut down, they're trouble. But that's belied by the charts - this started at the same time as the recession.

ReplyDeleteThe view from inside looks like a combination of 1) and 4). Namely, at any point in time a startup wielding a disruptive technology could appear and you need a war chest to either buy them out or bury them.

ReplyDeleteHere are some possible reasons:

ReplyDelete1) Safety/Fear of Calamity: When asked about what was the hardest part of the financial crisis, GE CEO Jeff Immelt immediately responded that is was cutting the dividend. CEOs/CFOs absolutely hate cutting the dividend, and keeping a lot of cash helps prevent this.

2) Opportunity #1: The world is experiencing a huge (one time only?) surge in development. Many, many parts of Asia, Africa, South America, etc. represent a massive opportunity for large American companies--and these companies want to have the resources available to take advantage of these opportunities as they arise.

3) Opportunity #2: The world is still unstable. Companies that keep cash in reserve may have the opportunity to invest the cash in very attractive opportunities. For example, Well Fargo was able to buy Wachovia--and DOUBLE their previous size--by maintaining a conservative financial policy in the years leading up to the financial crisis.

"The Great Stagnation"

ReplyDeleteCowen's latest attempt to fool people into thinking libertarianism is less devastating. It just so happens I'm up pursuing one of my most interested subjects, future advance of technology and how it makes employment and personal financial security riskier (and what is a good strategy/game plan/careers for college students and younger to deal with this risk).

For a while it was hard to find good research, books, articles, etc. But lately I've found some. Big score – "Race Against the Machine: How the Digital Revolution is Accelerating Innovation, Driving Productivity, and Irreversibly Transforming Employment and the Economy" by MIT management economist Erik Brynjolfsson and MIT computer scientist Andrew McAfee (and McAfee has a blog!). Quoting:

"The stagnationists correctly point out that median income and other important measures of American economic health stopped growing robustly some time ago, but we disagree with them about why this happened. They think it's because the pace of technological innovation has slowed down. We think it's because the pace has sped up so much that it's left a lot of people behind"

And of course, if it's the great stagnation that's so hurt the median family so badly, then why has the wealth and incomes of the rich absolutely exploded at the same time like never in American history?

And re. Krugman's latest post on Cowen:

ReplyDeleteI ain't the kind of guy that likes to socialism

I hang on to old primative ways

And I aint no fool for thinking that makes libertarianism look bad

Still Say's Law after all these years, oh still Say's Law after all these years...

This isn't much of a puzzle. If you talk to big companies in Silicon Valley (who are some of the biggest cash hoarders), the real reason why companies are not giving money back to shareholders (for the most part) is that they are waiting for Congress to pass a tax holiday to repatriate earnings to the US (as much of their cash sits in overseas subsidiaries). Because of past tax holidays doled out, corporations have learned to wait and be patient for such holidays in the future.

ReplyDeleteOnce the cash is back in the U.S., CFOs will give some of the money back to shareholders, but not all of it. They'll still keep a good chunk of it to be able to do mega-big M&A. It's bad corporate finance management in theory, but it provides the CFO peace and mind knowing that if the CEO says he/she wants to do some incredibly huge acquisition with cash, the resources will be there to do it, and most boards are too compliant to disagree with this strategy.

If you want companies to give back more cash, you should be cheering for activist investors. That's their mantra.

You're right, I did miss this explanation; I added it in the update.

DeleteBut is cutting corporate taxes really the only solution? We couldn't possibly just make this illegal?

DeleteIs there a finance solution to this problem? I recall a b-school case from the 1980s where firms had forex imbalances i.e. a long on GBP in Britain and short on US$ in the US. They would lend to someone in Britain and borrow from someone in the US and presumably hedge the forex exposure. Wouldn't a similar solution work for overseas unrepatriated profits? And if so, then as somebody would have thought of it already, it can't be the explanation for cash hoarding.

DeletePage 34 from the book in my first comment:

ReplyDeleteThere have been trillions of dollars of wealth created in recent decades, but most of it went to a relatively small share of the population...

This squares with evidence from chapter 2 of the growing performance of machines. There has been no stagnation in technological progress or aggregate wealth creation as is sometimes claimed. Instead the stagnation of median incomes primarily reflects a fundamental change in how the economy apportions income and wealth.

There has been no stagnation in technological progress or aggregate wealth creation as is sometimes claimed. Instead the stagnation of median incomes primarily reflects a fundamental change in how the economy apportions income and wealth.

DeleteWell, I'm not so sure you're right about that. Check out total factor productivity:

http://noahpinionblog.blogspot.com/2011/04/tfp-and-great-stagnation.html

That's actually part of the quote. It's the authors words not mine.

DeleteBrynjolfsson and McAfee talk about labor productivity growth (growth in GDP per worker). It is as follows:

1950s: 2.2%

1960s: 2.7%

1970s: 1.7%

1980s: 1.6%

1990s: 2.1%

2000s: 2.5%

From this you see a stagnation in the 70s and 80s, but back to the 50s in the 90s. And almost back to the roaring 60s in the 2000s. They also talk about how our GDP measure understates technological advance. And that in the last ten years the employment to population ratio shrank substantially – but that's a big part of their point: The technology has not stagnated; it's accelerated, but we've fallen behind in educating and training people who can really utilize it.

A lot of interesting points (and the books a very quick read; it's one of those "long paper" books):

1) "If wages can adjust freely, then losers keep their jobs in exchange for accepting ever-lower compensation as technology continues to improve...the economist David Ricardo, who initially thought that advances in technology would benefit all, developed an abstract model that showed the possibility of technological unemployment. The basic idea was that at some point, the equilibrium wage for workers might fall below the level needed for subsistence...We also now understand that technological unemployment can occur even when wages are well above subsistence" (pages 37-8)

2) For the future, he makes an interesting point using the chessboard story (one grain of rice on the first square, double on the second,...) At first the growth seems linear, not that impressive, but by the second half of the chessboard, it's astounding. Each new doubling at that point is a tremendous gain. With computing power it was like that at first to a large extent, but now each new doubling is a huge leap. And he gives the example of computer driven cars. This requires massive parallel processing, massive computation, and seemed impossible, or way off, to many even ten years ago. Now, he seems to imply, we're getting into the "neck" of exponential growth. Great stuff, very interesting.

And he notes exponential growth in software too: "Computer scientist Martin Grotschel analyzed the speed with which a standard optimization problem could be solved by computers over the period 1988-2003. He documented a 43 millionfold improvement...Processor speeds improved by a factor of 1,000, but these gains were dwarfed by the algorithms, which got 43,000 times better..." (page 18). Note how the software gains multiply the hardware gains and vice-versa. 1,000 times with one and 43,000 times with the other makes 43 million times!

3) "The threat of technological unemployment is real. To understand this threat, we'll define three overlapping sets of winners and losers that technological change creates: (1) high-skilled vs. low-skilled, (2) superstars vs. everyone else, and (3) capital vs. labor. (page 39)

I'm not an economist and I didn't think of this first (Angry Bear, maybe - I don't recall), but it makes sense to me: lower tax rates encourage profit-taking, relative to higher tax rates which encourage reinvestment.

ReplyDeleteCorporate taxes are not on revenue - they're on profit. So the higher the rates, the more incentive to treat revenue as a cost, thus avoiding taxes, while if the rates are lower, the incentive is more likely to be towards profit-taking, since less of it will be lost as taxes.

And reinvestment, although a cost, is also essentially an asset, which taxes are not. So tax rates influence the extent to which reinvestment is attractive as a cost. The higher the rate, the more attractive; the lower the rate, the less attractive (and the more attractive is profit taking instead).

If tax rates are low enough - e.g., essentially zero, which is the case for many corporations, cost cutting to maximize profit might become more attractive than increasing production. In that case, production capacity begins to get cut - or go unused.

Again, not my idea, but it does make sense to me.

>> This means we could induce companies to hold less cash by cutting corporate tax rates.

ReplyDeleteOr we could increase taxes on cash hoards. Bleed out the reserves, making it more advantageous to reinvest or pay out dividends.

Excellent question (and discussion) on why aren't corporations paying more dividends. Daniel Gross had offerred one other possible explanation for hoarding cash back in the days when Microsoft had not yet paid dividends. Suppose there were a lot of employee stock options not yet exercised but in a position where they might be at anytime. Then the corporation might be holding cash as a precautionary motive just in case that employees decide to quickly exercise these options. I have no idea whether this model would come close to explaining the amount of cash we are talking about but I thought I would add this to your interesting list.

ReplyDeleteIf you are a manager with unexercised options I assume that you would not participate in a distribution of dividends now but if the company hoards cash that increases the value of your options. Widespread stock options among senior management could be a reason for low dividend payouts.

DeleteThe same effect (for the manager w/ the options) would be for the firm to buyback stock. I think most large firms with employee option programs already do this at least to cover the options they have issued. I don't think this explains the cash hoarding.

DeleteMost of the cash is in tech companies, and the reason they hoard cash is to buy their competitors. Most of Cisco's cash flow goes to buying up potential competitors, for instance. Amazon doesn't hold much cash because it would be very difficult to reproduce Amazon, not hard to create new handset or search engine co.

ReplyDeleteWhy don't they just do LBOs, with interest rates at such historic lows, not to mention the tax breaks, and also the inefficiency of building up and holding all those cash balances in advance?

DeleteCollateral is an issue thus making LBOs difficult. TechCos typically don't have the best assets to be used as credible collateral. LBOs usually involved hard assets, like property. Even IP can be tough to borrow against, especially to get the 90% D to E ratio on an LBO.

Deletethat begs the question, why do tech assets look bad. Kraft, Phillip Morris, Hostess, are really just collections of brands, why are these better than patent s?

DeleteThe archetypal LBO is crushed by a recession or tech change. To reduce this risk, They are leveraged to a product revenue stream with high entry barriers, inelastic demand, and/or low rate of change (think corn flakes, cigarettes). The degree of cashflow certainty dictates the degree of leverage. Rapid technological change is a real killer (like shale gas which killed TXU) because its so unpredictable.

So why not leverage up Apple, or Microsoft. Is Microsoft really a "utility"? I would say rapid tech change makes these companies unlikely LBO candidates: within the maturity of the debt that would finance the LBO, we can forcast some new "killer" technology. Hence these companies need cash to insure their survival (buy buying fast growing new tech companies).

Yeah, this is basically my explanation #1.

DeleteIt is essentially #1, but #1 also shades into the definitional (indecision due to uncertainty). Details matter, but I know economists are also formalizing answers so the details disappear, which is perplexing to non-economists.

DeleteOne idea comes out of my brain: the "keretsu" company, associated enterprise in Japanese. The "keretsu" companies borrow money from related banks with extremely low interest rate because they are big and being trusted. Then they lend money to affiliate companies (even other "keretsu" companies' affiliate company) .Those "keretsu" companies act like finance holdings, as a result, they need additional money reserve to avoid bankruptcy due to this kind of business. The "Keretsu" company is the combination of bank and corporate. In China, a lot of famous or state-owned enterprise do this kind of business because banks do not trust small business (so that the credit spread is too high to afford ). They substitute for banks to finance the industry, as a result, the bank tends to provide more mortgage loan because they believe ....they really "understand" the real estate market.

ReplyDeleteI think this may refers to that, banks can not understand the industry better than the "keretsu" companies. The "keretsu" company invests those affiliate companies and only takes low (about zero) return from (maybe preferred stock) dividends. When investors hold "keretsu" company's stock, it is like to invest in a combination of common stock and saving deposit. How sweet they are! I can only reinvest them with zero-rate saving deposit if they pay dividend, uh? At least I won't have reinvestment risk at all.

Having lived in Japan too long, I vote for number 2*. Over here, the shareholder has always had far less power over companies than their investment would indicate they should, and management thinks of their company as really being "their company". I'm under the impression that in the US, a lot of stock is managed by funds, investment managers, whathaveyous, and the individual investor doesn't get involved, thus giving management a freer hand. So the US is turning Japanese, at least in that sense.

ReplyDelete*: 2) The link between management and shareholders has totally broken down. Management is acting in their own interests instead of shareholders', and shareholders haven't really noticed this, possibly because dividends were so low in the 1990s and 2000s.

During the the crash, there was a flight to safety in values stocks often measured in book to price.

ReplyDeleteThe fundamental issue became return of capital, instead of return on capital.

Questions like, what kind of assets is this company holding? What kind of risk are they holding? Can spook investors.

Having a fat cash pile is a way of both staying appealing to risk averse investors, but also preparing for the moment, where cash will be spent competitively. Sort of a "cash arms race" if you will.

While the indexes have been outperforming, I don't believe most managers see that they are in the clear for spending. Perhaps another 6-12 months of stability and modest growth will give them the confidence they need.

I do believe Euro + Sequester, do have adverse effects, as well as the potential for new tax regimes (and the unseen effects of new changes like ACA..) All of these pieces form a larger uncertainty picture.

Having a fat cash pile is a way of both staying appealing to risk averse investors, but also preparing for the moment, where cash will be spent competitively. Sort of a "cash arms race" if you will.

DeleteThis makes sense...basically a combination of reasons 1 and 4 from my list...

the potential for new tax regimes

But this is all upside, right? Nobody would dream of increasing corporate taxes now, and most people want them cut. As for dividend taxes, this would only make companies hold cash if they thought the taxes were going down, not up. And I don't see how capital gains taxes would affect it much either way.

Um...

DeleteHow about I say this... maybe spending cuts could effect output and the economy... and maybe, just maybe, tax rates or capital gains rates in some strange crazy universe could effect the market short term.

i know that's antithetical to some people religions... but I'll just throw it out there... maybe...

Or in the vaguest terms possible, how potential, future austerity, in some form, or another, should/must/will occur, even slightly..

uncertainty... no?

Not sure I get this...you're saying that at some point taxes must go up, and when they do it'll be a drag on growth, and since we don't know when this will happen, it's causing uncertainty for businesses?

DeleteI'd buy that.

At "some point" = debt to GDP is getting too high, all signs point to some form of "austerity" on the short to medium term horizon.

DeleteWhat will this be:

"can kick for a while (4 years) followed by X"

"spending cuts soon (sequester)"

"increased spending soon, higher taxes soon"

"slightly decreased spending soon, slightly higher taxes soon (micro bargain)"

"grand entitlement reforms after the midterms"

etc... lots of different outcomes..

I'm sure you can think of more

just to add: the "cash arms race" is often a cache for mergers and acquisitions. The goal of tech startups is often to get bought out by oracle, google, or whomever. Cash is hard to beat in a merger. This dovetails with #2. But I don't agree that the "link between management and shareholders has totally broken down" because this presupposes it was there in the first place. It is usually pretty weak. Oh, there are exceptions where management owns a lot of shares, but my experience is that once you are sufficiently rich, incentives like stock don't do much. At some point, it becomes more about power, prestige, and bragging rights.

ReplyDeleteThere is another part of Cowen's post that interests me. Cowen says it does not matter if companies hold "cash" because it just means that they have loaned it to someone else who will either spend it or lend it further along the chain. Ultimately the money must be spent by someone since it cannot be endlessly passed along the chain. Given the speed of transactions and the fact that even idle money sitting in a bank has been loaned to the bank, transaction lag is not going to create much delay. Idle bank deposits might show up as excess reserves at the Fed but I assume that this counts as a loan to the government which can (indeed must) be spent by the government. In effect Cowen says the money does not disappear.

ReplyDeleteKrugman seems to suggest that the money disappears. This seems to be the central difference between Krugman and the Ricardian Equivalence guys like Cochrane. If Krugman is right, where does the money go?

Easy question. Money is not conserved.

DeleteMoney is not conserved.

DeleteI'll bite. If it is not conserved - where is the sink hole?, it what point does it disappear?

Companies are holding (T-Bills)

DeleteThe money is going into T-Bill Auctions which the Fed is also buying.

More and more T-Bills are being created and bought. What does this mean?

The real question is what happens to the money when:

A) The fed stops buying T-Bills (or will it, ever?)

B) Interest rates go up

A) would mean a dirth of demand so ---> higher rates (the T-Bills will be worth less so money will be destroyed)

B) see A)

So then what happens if 0 rates forever?

Absalon, Asset price fluctuations. Asset price deflation will ultimately be the money sink.

DeleteI'll bite. If it is not conserved - where is the sink hole?, it what point does it disappear?

DeleteMoney disappears when banks reduce lending and hold more excess reserves.

Real income disappears when economic activity decreases.

Money disappears when banks reduce lending

DeleteIs there any economic difference between a bank holding t-bills versus holding the same amount in excess reserves? Does money disappear in both cases?

Yes. Not exactly the same, but very similar.

DeleteI ask a rhetorical question: how does the market value a company's common stock ? A non-dividend-paying company is valued by estimates of it's growth, where a dividend-paying company is at least partially valued by it's yield. It is also the case that a dividend paying company often appears to be less of a growth opportunity. So, bottom line, one prefers to be valued at a growth company's P/E than as a reflection of one's dividend yield. I offer AAPL as the poster child for that calculation.

ReplyDeleteHow about this, firms can write off interest on debt only to the extent of dividends they disperse?

ReplyDeleteWouldn't it cause a drastic move away from debt finance to equity finance?

And why would we want that?

DeleteManagement gets compensation (like investment fund managers) based on the asset (especially liquid) size of their company. Stock options are worth more when there is plenty of cash to redeem the options. Stocks change hands so quickly that dividends are ignored. And there is so much offshored money in subsidiaries (just look at Dell), that hoarding money overseas tax free beats bringing it back to the US. THE ANSWER IS NOT TAX FREE REPATRIATION. The answer is a tax on offshore holdings.

DeleteThat would level the costs of repatriation without starving our treasury. And ultra-low inflation rates actually encourage hoarding and wage suppression. CEO's would look for new opportunities rather than engage in rent-seeking if their principal was being eroded by inflation.

Once bitten, twice shy. Corporations just saw every over leveraged company get taken to the woodshed post Lehman, who wouldn't build a little cushion in response? particularly with a lot of questions out there around Europe and fiscal austerity still hanging unresolved.

ReplyDeleteTax policy is a rabbit hole, having a corporate tax at all is not good policy, but it does seem that allowing companies to repatriate cash tax free equal to their increase in investment spending would be an idea everyone could support.

total cash returned to shareholders has been increasing rapidly post financial crisis, this trend is likely to continue, and will likely go along way to answering your question looking back in a year or two.