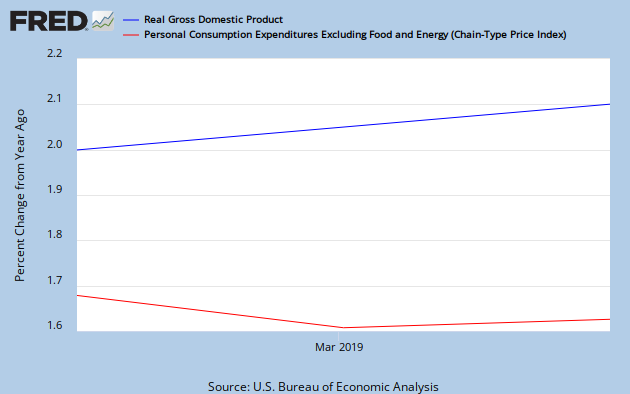

Without a doubt, QE has been an incredible boon for financial markets. Backed by QE3, the SP500 stock index has risen by more than 12% year to date. Yet in spite of this increase in the stock market, overall real economic conditions remain relatively stagnant. Year over year inflation as measured by the core PCE price index ticks in at only 1.2% YoY, and last quarter's real GDP grew by only 1.4% YoY. This disconnect is a bit unsettling, because it suggests that bullishness in the stock market has failed to translate into broader growth. On this basis, some commentators, such as Frances Coppola, have argued that quantitative easing does nothing for the broader economy and worsens economic inequalities. But this concern can be reduced to an even simpler question: Has recent stock market growth just been a bubble?

There are a few reasons why this question is important. First, people make a lot of noise over the financial instability hypothesis that monetary policy is just fueling speculative excess. So for the sake of practical monetary policy, it matters if signs of a bubble are appearing. Second, if it can be shown that we are not in a bubble, and that recent financial market movements are based on fundamentals, this means that monetary policy is passing through to the economy. It's not just some scheme to enrich the wealthy. Moreover, the tools that we develop to analyze this issue can help us determine in the future if certain monetary policies are passing through to the economy. Third, analyzing this issue leads to some more insights on how finance and macro can work together. While I am sympathetic with Scott that finance should be kept out of theories of money, given that financial indicators function so well as forecasts, it would be a shame to not use as much data from the financial markets as possible.

Because this is a highly charged question, I want to make the conversation as concrete as possible. When I talk about a bubble, I don't just mean "stock prices are high". Rather, I want to define a bubble as when stock prices are "out of line" with the fundamentals of the underlying companies. What this means is that if China blows up next year, and the price of stocks fall, that doesn't mean the bubble popped. A blowup in China is an exogenous event that would change fundamentals, and prices would adjust as a result. The type of bubble that I'm talking about is a noise trader, "beauty contest" bubble, in which people go into a frenzy bidding up the price of securities on the belief that everybody else will bid them up as well.

So let's start by talking about how monetary policy affects stock prices. On first approximation, the value of a stock should be equal to the present discounted value of all dividend payments. Sure, there's excess volatility around the edges, but this simple model of cash flows is still accurate on average. In doing so, it gives us two ceteris paribus predictions about stock prices. First, a stock price should go up in response to higher expected future cash flows. Second, a stock price should go down with higher expected real interest rates, because a higher real rate reduces the discounted value of future cash flows. These are the two main channels through which monetary policy impacts stock prices. Monetary policy can either (1) raise the cash flows by improving the economic environment, or (2) lower the discount rate by maintaining an extended period of low real rates.

These two channels split quite nicely into a positive and negative take on the effect of monetary policy. If monetary policy raises stock prices because of current and future cash flows, that should be seen as a good sign of a recovering economic environment. This corresponds to "the Fed is improving the fundamentals of the economy." On the other hand, if monetary policy affects stock prices only through a lower discount rate, that is just a sign of an "immaculate conception", with stock prices rising without an improving economy.

Most market monetarists believe it's the former, whereas some fiscalists have made an argument that it's just the latter. But here's the kicker -- we should be able to distinguish the two by looking at the actual earnings data. By comparing the earnings of companies and the stock prices, we can actually make concrete the discussion about whether the stock market is in a bubble. In particular, we can distinguish between the two stories by looking at price to earnings ratios, or the ratio between the price of a stock and the earnings per share -- both in the trailing 12 months and 1 year forward estimates. If the fundamental story is correct, then we should observe that the price to earnings ratio stays relatively constant. Yes, stock prices are rising, but that's only because earnings are stronger. If the speculative excess story is correct, then the price to earnings ratio should be rapidly rising as the price is bid up, but the underlying earnings remain unchanged.

On this note, it doesn't look good for the bubble mongers. Below I have trailing 12 month and 1 year forward price to earnings ratio plotted for the SP500 index as a whole. The index P/E ratio is calculated through a market capitalization weighting process of the underlying index securities. What this shows is that, right now, stocks are quite cheap. The trailing 12 months PE ratio is at 15.5, a far cry from the heady tech bubble days with a peak P/E of 30 or even the moderate 2002-2008 period when the PE ratio tended around 18. The trailing 12 months ratios mean that prices aren't out of line with past performance. The fact that forward ratios are also relatively low and near the trailing ratios indicates that stock prices aren't up on the back of extremely optimistic future forecasts. Even though high PE ratios aren't sufficient conditions for a bubble, they're certainly necessary ones. If this is a beauty contest, it's awfully fair.

The moderate P/E ratio signals that people are not overpaying for performance. This isn't the 1990's -- market participants are not basing valuations off of overly optimistic views of future earnings. Rather, people are just paying reasonable amounts of money to buy into each company's earnings, resulting in reasonable stock prices.

Now, in my analysis above I glossed over one more channel that's relevant for the financial stability debate. It's possible that the liquidity provided by monetary policy encourages people to take riskier investments because they're "reaching for yield." But we should differentiate two versions of this hypothesis. The first is that people are over weighting risky sectors at the expense of safe ones. But this should not be a concern of policy because it's not systemic. When the reach for yield reverses itself, some stock investors will win, others will lose, and while there may be blood, policy makers need not wash their hands. On the other hand, if people are just pouring their money into stocks in general because they are dying for yield, then policy makers might be concerned. But the low PE ratios belie this hypothesis, so policy makers can still rest easy.

So if equities aren't a bubble, this means that the recent rise in stock prices corresponds to better fundamental performance for these companies. Therefore we should expect a pass through to the overall economy and for conditions to improve. Monetary policy was certainly not futile.

This can also give us a sense of where the economy is going as well. From the P/E ratios and the actual index level of the SP500, we can back out a quarterly earnings index -- both expected future earnings and actual trailing twelve months. By comparing expected earnings with the actual earnings one year later, we can actually evaluate how accurate forecasters were. Surprisingly enough, post dot com bubble, earnings forecasts were pretty accurate during normal times, and only when there was a policy failure (in 2008), was there a significant deviation. This suggests that earnings should continue to grow, and that the real concern shouldn't be on whether the stock market is getting frothy, but on whether overly contractionary monetary policy will send the recovery off course.

So if you want to avoid those bad, unequal, configurations, then you will earn my respect as you fight for targeted fiscal interventions. Just keep your hands off my monetary policy, because the most dangerous idea you can have is that it doesn't matter.

Update: Fixed some typos. Changed "monetary policy" in fifth sentence of first paragraph to "quantitative easing"

Why should one think that a stockmarket bubble is the only possible bubble? Bubbles get blown up in asset markets that may not even figure in every day discourse. In the last financial crash it happened in the real estate and credit default swaps, to begin with. The only way of sensing a bubble is to measure money correctly.

ReplyDeleteSee the two measures of money in http://www.philipji.com/item/2013-07-03/two-measures-of-money-supply-1981-to-may-2013

Sorry, but I am not buying that "economic" conditions were stagnant. More like the Government data machine is in error and undercounting growth, alot to do with the 2011budget deal from what I am hearing. Inflation is a poor indicator because the market has to clear before inflation will rise in a high supply world.

ReplyDeleteSome impressive benchmark upward revisions to come and will then cause people to nod their head. The surge in tax receipts is the real clue.

You said: "You can have severe inequality, a high labor share". I guess you wanted to say "a low labor share". Indeed, one of the possible causes of a relative price to earnings stability might well be the changes in the capital/labor shares, and NOT a genuine increase in both the prices and the earnings.

ReplyDeleteThe point is important because one can perfectly wonder where all these higher earnings are going to.

Your data base seems to demonstrate that fundamentals are improving and, as a consequence, the Dow Jones is in line with them. But they even suggest that the Dow Jones falls short, because the lower real interest rate has also been reduced. Are you suggesting that there is more increases in the months to go?

Fixed. I mean to say low labor share.

Delete"Without a doubt, QE has been an incredible boon for financial markets."

ReplyDeleteWhat a logical sleight of hand. The train of thought seems to go somewhat like this:

1. Stocks are not in a "bubble" because fundamentals (earnings) support current valuations;

2. Therefore ("without a doubt") QE has not only been an incredible boon for financial markets, but for the economy as a whole.

Even if we accept 1. as fact, at best the author has established is some temporal correlation between QE and the performance of the market (and/or the economy).

It strikes me that if QE has not raised stock prices above a price justified by current fundamentals, then the main channel of QE is not working (at least the channel Bernanke thinks should be at play---the wealth effect---by increasing (select) asset prices above fundamentals).

Also, this sentence is flawed:

"Second, a stock price should go down with expected real interest rates, because a higher real rate reduces the discounted value of future cash flows."

The first clause is in direct competition with the second.

If you want to impress me with something original and insightful, come up with proof and not merely an inappropriate conclusion wrapped around a bit of shaky correlation, that QE is actually *causing* these purported effects.

This is the same reaction I had. If equities are actually priced according to fundamentals, and QE had something to do with driving up the equity price level, then the conclusion would seem to be that QE is needed just to get markets to correctly price what they trade. That's an interesting argument, but I think it would need more evidence?

Delete"If equities are actually priced according to fundamentals, and QE had something to do with driving up the equity price level, then the conclusion would seem to be that QE is needed just to get markets to correctly price what they trade."

DeleteNot exactly. The argument *seems to be* that QE improves the economy and therefore the fundamentals and therefore the stock prices.

I think that's short-sighted and far-fetched and certainly this column does nothing to prove it.

I see two possibilities:

1. QE improves economic "fundamentals" (definition required). But, this seems highly inconsistent with low(er) real interest rates. In the case of "improving economic fundamentals", the prospect of future economic growth should result in *higher* real rates; or

2. QE *artificially* reduces real interest rates, but not overall "economic fundamentals" and therefore translates into higher current stock valuations (even if projected earnings are constant, lower real rates translate into higher current stock valuations).

This tracks closely (but not precisely) the author's own version:

"These are the two main channels through which monetary policy impacts stock prices.

Monetary policy can either (1) raise the cash flows by improving the economic environment, or (2) lower the discount rate by maintaining an extended period of low real rates."

Number 2 above is a bit of sophistry. What is an "extended period"? Are these interest rates sustainable or would they be reversible over time? That's the key. If the Federal Reserve succeeds in *temporarily* lowering interest rates (and therefore increasing stock valuations) but this *temporary* situation must inevitably be reversed, is that the creation of a "bubble"? By my definition, a temporary and artificial as opposed to a permanent reduction in rates would be.

The author defines a "bubble" as follows:

"Rather, I want to define a bubble as when stock prices are "out of line" with the fundamentals of the underlying companies."

That's not entirely helpful because "fundamentals" are not defined. I would define "fundamentals" as current and projected earnings discounted by current and projected interest rates that are *indefinitely* sustainable and not merely *temporarily* sustainable (or even for "an extended period") because of artificial props introduced by the Federal Reserve (or temporary non-market props introduced by others).

I don't think there is any question the Federal Reserve can (temporarily) increase stock prices by (temporarily) reducing real interest rates.

Economic sophistry nearly always depends on arbitrarily selecting a time frame that is favorable to one's hypothesis. The only exception here is that it is a rather amateurish attempt.

There is absolutely no causal connection shown here between QE and improved economic conditions in the real sense. Temporal "cosmic synchronization"may have something to do with art, but certainly not science.

In other words, given the 0% interest rate policy at present, a simple 0.5%, never mind a 1% point increase in interest rates will have a massive impact on the company valuations, "instantly" creating an asset bubble when companies' valuations are cut by 30% or more, while in reality the earnings projections remain the same.

DeleteYichuan,

ReplyDelete"some commentators, such as Frances Coppola, have argued that monetary policy does nothing for the broader economy and worsens economic inequalities".

I have never, ever suggested that monetary policy was useless and/or harmful to the broader economy. Nor would I. Managing the quantity and price of money is a reasonable thing to do in an economy where the sovereign is the monopoly (or near-monopoly) supplier of money.

To equate QE with monetary policy is absurd. QE is only one among many monetary policy tools. My considered opinion of QE, which I have stated on several occasions, is that it is a good response to a deflationary crisis such as we had in 2008/9, but that it cannot offset contractionary fiscal policy and has toxic effects on the broader economy when used long-term. I am not the only person who has noted QE's distributional effects (it does worsen inequality, because it benefits asset holders at the expense of those who do not have assets) and its tendency to raise commodity prices. When those commodity prices include oil, then QE is toxic for Western economies.

There is no doubt in my mind that QE is partly responsible for the high and rising oil price since 2009, and it is possible that recovery has been elusive because of the effect of high oil prices on economies dependent on oil imports. I'm pretty sure that's the case in the UK: rising energy prices plus sterling weakness was in my view largely responsible for the failure of the nascent recovery at the end of 2010.

Good point -- I should have been more careful. I guess what I mean t to say was "the marginal monetary policy action at this juncture". I did not mean to mis-represent your views. I apologize for that.

DeleteBut I guess my point on the stock market still goes towards your concern that QE only has those negative distributional impacts and cannot affect the broader economy. I remember you arguing many times that monetary policy's transmission mechanism is sorely broken, yet by the measures of earnings it's clear that growth has been steady.

Many market monetarists point to the stock market as a test for why monetary policy works. This post is meant to point out why that's still a valid point.

I also think you're confusing supply and demand issues when you talk about oil prices. This will be something I address in a future post.

FWIW, I don't think that the stock market is in a bubble. But investment earnings are not a reliable indication of growth.

DeletePlease don't tell me that rising world oil price in an economy whose industrial production is dependent on oil imports is a "demand" problem.

It's certainly a long term structural problem. It's just that I'm not sure if it's the most pressing issue right now.

DeleteTo be honest, I haven't done too much thinking about oil prices, it's just that my gut instinct is that it's not the major barrier facing the world right now. I could be persuaded by evidence to the contrary.

I used to think the oil price wasn't that important any more....until I did some research into the reasons for the failure of the UK's nascent recovery in 2010. There was over 16% inflation in energy prices, for a variety of reasons including high world prices for oil and gas, the weakness of sterling, new green levies on energy and a VAT rise. To my mind that is a sufficient explanation of falling industrial production from Q4 201 onwards, although the Eurozone crisis didn't exactly help either.

DeleteThe UK wasn't the only country affected either. The ECB raised interest rates in 2011 to choke off inflationary pressure particularly in Germany due to rising oil prices. There is little doubt that this contributed to the collapse of Greece.

It may be that for some reason the US is less vulnerable to oil price changes. It would take a great deal to persuade me of this, though.

I agree there is a long-term structural problem with energy. But there was an oil price spike in 2008 followed by a collapse (due to the financial crisis). The oil price then climbed sharply from Q3 2010 onwards to new highs, and remains above where it was in 2008. I don't think these changes are due to a long-term trend.

Professor Coppola: I commented below that transferring large amounts of wealth from the workers to the 1% could lead to a large rise in the stock market, without helping the "broader economy" -- but that this is NOT a bubble, because it could persist indefinitely (it persisted for hundreds of years at a time during the Middle Ages).

Delete"By comparing the earnings of companies and the stock prices, we can actually make concrete the discussion about whether the stock market is in a bubble."

ReplyDeleteAccounting profits are largely a fiction that misrepresent true earnings/cash flows of a company. Yes, stocks tend to trace P/E ratios, big whoop.

You say a stock's price is based on dividends, and presumably by extension for 0 dividend payout companies this is represented in general by earnings. But the DCF view is not sufficient for non-debt, non-annuity assets.

If discounted earnings were the only determinant of value and the altering perception of the trajectory of those cash flows were responsible for stock price fluctuations, life would be a lot easier. But stock is not debt. Shares have balance sheets with assets that contain values that aren't driven by cash flows that undermine DCF valuation.

There is most definitely a bubble. The Fed is taking trillions worth of assets out of the dollar-denominated financial marketplace and forcing participants to scramble into big, liquid dollar markets, like S&P.

And you can always find some news that can be labelled as an exogenous event that alters fundamentals, so you've set up an unfalsifiable premise for your claim that there is no bubble.

If, for example, S&P was falling right now, you could claim it's due to India and China sufferinng. Or if it was last year you could have claimed it was geopolitical stuff. There's _always_ some event that you could point to and say "see, no bubble, exogenous event, so fundamentals changed and price adjusted. market is efficient."

And as many people have pointed out, EMH is nothing but a tautology.

Mr. Wang,

ReplyDeleteYou may be missing or glossing over a critical point. The reasonableness of a P/E or any other multiple is a function of not only current earnings but (perhaps more so) the expected growth path. 15x is a "fair" multiple when the economy is not recovering from a deflationary depression *and* facing deflationary headwinds. To apply the same multiple today is to expect corporate earnings to grow at largely late 20th century pace in the intermediate term - which seems uncertain at best (many better informed than me folks have articulated those headwinds quite well - demographics, deleveraging, assymetrtic future risks around cost of debt service and taxation, declining ability to increase non-US share of earnings, etc).

Instead, what seems to be going on is the logical repricing of all risky assets given long-term real rates that are 300 bps lower than the 1990s and you would be right. Naturally, if bonds are offering certain risk adjusted returns, (correlation considerations aside), stocks should reprice accordingly. But that is precisely the "latter" of the two arguments.

This is a great point -- it's also worth noting that earnings 'quality' has been questionable. Corporate profits have been driven more by expense reduction than by revenue growth. If expenses can mostly be attributed to labor's share of income, this is certainly not a good sign for the economy.

DeleteP.S. Sorry for the two posts, I am new to the comment thing. To be clear, I don't mean to suggest we are in a bubble. I don't think there is anything pre-destined about long real rates of 2-3% - we may well be in an effectively permanent (for all practical horizon purposes) low return environment, largely due to oversupply of capital. But I don't think the evidence you site for the primacy of the "real economy channel" is sufficient.

ReplyDeleteThe stock market might be overpriced by 20% and that would just be business as usual and not a bubble. The bubbles we should be concerned about are in long bonds and the derivatives markets and Fed policy has contributed to both.

ReplyDeleteYichuan,

ReplyDeleteIf equities were discounting solid future earnings growth in April of 2013, why was the 10yr at -1% real?

This post by Tyler Cohen, particularly the last paragraph, is relevant to my question above.

ReplyDeletehttp://marginalrevolution.com/marginalrevolution/2013/08/asset-prices-and-interest-rates.html?utm_source=feedburner&utm_medium=feed&utm_campaign=Feed%3A+marginalrevolution%2Ffeed+%28Marginal+Revolution%29

It's dismissive articles like this or the ones denying the existence of non-bond market based inflation that sometimes makes no opinion painful to read. It's like when creationists insist that earth was formed thousands of years ago or that the complexity of life is only possible through a creator. It flies in the face of the preponderance of evidence. It's like when Krugman in 2008 said that 150 oil wasn't a bubble or speculation, but good ol' supply and demand. When oil fell to $40 a year later, did demand fall that much too? no, nitwit. it was a bubble

ReplyDeleteThough I agree oil rose to unreasonable levels in 2008, the demand and price need not have a linear relationship. Buyers at the margin may bid up / down prices much more quickly than the rise and fall of overall demand.

DeleteIt has been well-studied that the rise in corporate earnings has been due to layoffs and other expense reductions. Sales have been stagnant; the P/S ratio is the highest now since the 2007 market peak. That says "bubble".

ReplyDeleterecord corporate profit is caused by the junk bond bubble, as corporations borrow record amount of money to buy back their own shares.

ReplyDeleteDoes this take into account the fact that corporate earnings are not entirely dependent on the US economy? Since corporations can make stuff outside the US, and sell stuff outside the US, and even keep their cash outside the US, "QE is good for corporate earnings" does not necessarily translate to "QE is good for the US economy as a whole."

ReplyDeleteYour corporate earnings calculations are not comprehensive enough in that you reference only two metrics, both of which are closely managed by corporations in their financial reporting. If you were to consider earnings over a longer horizon (eg, CAPE 10), you'd reach a different conclusion. Additionally, corporate earnings are 70% above their historical rate. If you believe that is a number that can be maintained, then your analysis is reasonable, and I'd agree we're not in a bubble. But if earnings mean revert, then clearly we're in a bubble (presuming one believes that 70% above trend constitutes a bubble), and the market will tread water (at best) or decline over some time period. As a final point, the bulk of earnings growth is courtesy of the financials- if you were to remove those from your earnings calculations, S&P earnings would have declined over the past 12 months, not grown. This is where QE has a material earnings impact- the TBTF enterprises are able to leverage QE into profits, which are not sustainable as QE attenuates.

ReplyDelete"On this basis, some commentators, such as Frances Coppola, have argued that quantitative easing does nothing for the broader economy and worsens economic inequalities. But this concern can be reduced to an even simpler question: Has recent stock market growth just been a bubble?"

ReplyDeleteNo, these are two different questions.

My thesis is that the core problem is *maldistribution of wealth*. If quantitative easing transfers wealth from the poor to the rich, then the stock market growth is *not* a bubble -- since it can persist permanently. The stock market growth is then simply a direct effect of worsening economic inequality -- every rise in the stock market is a transfer of wealth from the 99% to the 1%.

There is AMPLE evidence for this, as corporate profits rise, wages drop, and employment drops.

"stock market growth is *not* a bubble -- since it can persist permanently. "

ReplyDeletea permanently high plateau