Neojaponisme is an English-language magazine about Japanese pop culture. In the latest issue, editor W. David Marx interviews me about the various myths and misconceptions that many Westerners (and some Japanese people) have about Japan's economy. Here is the part where I lay out most of the myths:

Can you help debunk us the main myths of the Japanese economy?

Myth #1: “Japan is an export-dependent country.”

Actually, exports are a smaller part of Japan’s economy (16%) than that of most rich nations’ (though bigger than the U.S.). Also, Japan hasn’t had a big trade surplus for a while.

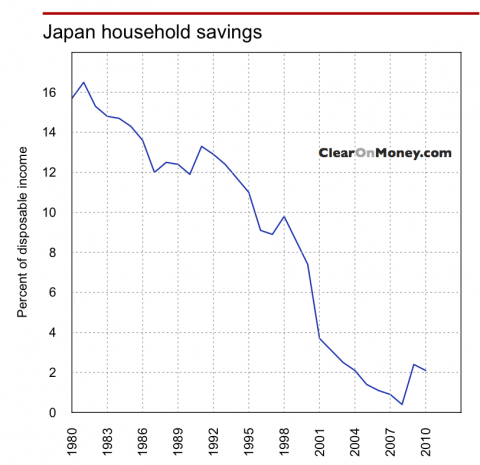

Myth #2: “Japanese households save a lot.”

This used to be true, but isn’t true anymore. The household savings rate nearly hit 0% in 2008 and is only around 2% now (America’s is around 5%).

{kind=link}

Myth #3: “Japan is a top-down economy guided by industrial policy.”

This used to be true, but isn’t anymore. The influence of METI (formerly MITI) has been curbed substantially. The Ministry of Finance still has a lot of power over banks, but this is true in other rich countries too and is generally what happens after a big banking crisis.

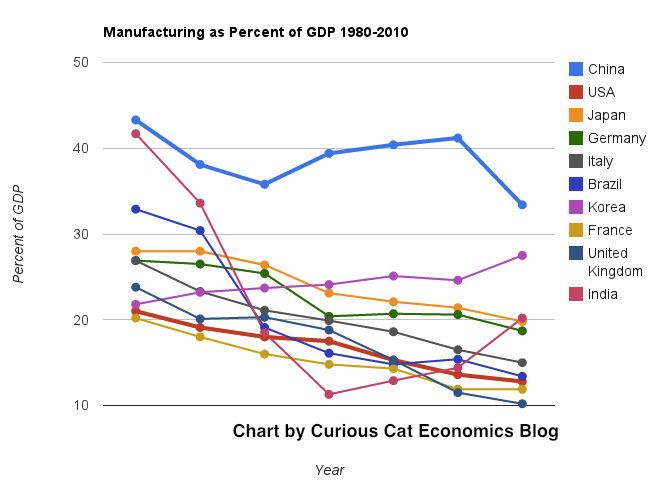

Myth #4: “Japan is a manufacturing-based economy.”

Manufacturing makes up slightly more than one-fifth of Japan’s economy, which is more than most rich countries (only Germany and Korea beat it), but is a lot less than most developing nations. India, for example, is now more manufacturing-intensive than Japan.

{kind=link}

{kind=link}

Myth #5: “Japan has lifetime employment.”

Sure, for the top half of the workforce. For everyone on the bottom, it’s a constant struggle with little hope of big raises or promotions. And among those with so-called “lifetime employment,” maybe half are in danger of losing their jobs to layoffs.

Myth #6: “Japanese companies aren’t innovative.”

This is just wrong in so many ways, I could write a book about it (and maybe I will).

Myth #7: “The Japanese buy government bonds out of patriotism.”

Unlikely. They probably buy Japanese government bonds out of fear, pessimism, and a lack of knowledge of good alternative investment opportunities.

Read the whole interview here! I also talk about regulation, innovation, labor markets, monetary policy, and a bunch of other stuff.

The comments section over there is really good right now, too.

ReplyDeleteOut of curiosity (and I posted this over there too), but what did you think of the housing stock over in the Tokyo area when you were living there? I didn't see a lot of home residence full house central air conditioners like you see here in the US.

Yup, only now are a few houses being built with those. But hey, it's better than friggin' NYC! I might soon buy some rental property in Japan, so I'm looking at that pretty carefully...

DeleteRegarding #1 and #7, it has always been the case that exports were a small part of GDP, although they did used to have a big trade surplus. On 7, I think you are discounting the role of patriotism too much, although the factors you mention are there for sure.

ReplyDeleteFunny you are thinking of buying rental property there, but do not mention at least in the main part of the interview the long decline of the real estate bubble, the only bubble every to go down more slowly than it went up, a great mystery. Do you have any explanations for that one, and do your contemplations mean that you think the long decline is finally about to be over?

Barkley Rosser

Hey, Barkley! Do you have any evidence of patriotism playing a role in Japanese asset purchases? That would be pretty neat.

DeleteJapanese rental properties have essentially no resale value, so I'm not worried about that. My reason for wanting to buy a rental property is a long story, but basically rental yields are quite high, and it's just a way to make a little extra cash.

Certainly cannot be definitely proven, however, even when prices are similar they are much more likely to buy goods produced in their own country than imports across many sectors. An example besides their own bonds is Japanese rice, although there is a lot of protectionism of that. Nevertheless, the favoritism to buy rice goes beyond the protectionism. The price is very high and political support for that protectionism extends far beyond the tiny percentage of the population that are rice farmers.

DeleteThere is also the phenomenon of keiretsu loyalty: someone working for a company in a keitetsu will tend to buy goods from other companies in that keiretsu. Most of the Japanese I know are very patriotic, even if they tend to be low key about it, and very proud of Japanese products.

BTW, interesting that price/rent ratios are now very low in Japan. The bubble has been coming down for a long time, probably now way overshooting on the downside. It was the late Charles Kindleberger who first pointed out to me the unique nature of the real estate bubble decline a long time ago. Might be a good buy by now.

On the matter of patriotism, or some might prefer to say "nationalism," among the Japanese, the stories about the death of Hiroo Onoda who did not surrender until 1974 from WW II are a reminder of how intense that can be, and while they tend to keep their heads down, is deeply embedded, particularly among the older generation who are those most into buying bonds. I know, Noah, that you have spent a lot of time in Japan, but this may be a matter of age. I suspect you have not had the sorts of conversations I have had with older Japanese, who one must get to know, and preferably have had some drinks with, before one can probe such issues more directly, but the nationalism runs deep.

DeleteOn the matter of buying bonds and the motive of "fear," well on that it may be hard to separate things out. We know in general that in most countries "home equity premium" is a very real phenomenon, and in most it is tied very much to fear of foreign exchange markets and foreign assets in general, although one could probably say that it is partly a matter of ignorance as well regarding the benefits of international diversification of portfolios. So, I am sure there is a lot of that among buyers of Japanese bonds, but given how much lower the yields were for so long compared to those on foreign securities, and while not so much lower now, they are still the lowest in the world, I think, one should not rule out some greater element of nationalism/patriotism in their purchases on top of the usual fear and ignorance one finds in most such markets, although, again, this cannot be proven.

Also on the matter of the peculiar behavior of Japanese real estate, again, this appears to be the only bubble in world history that has declined more slowly than it went up. There remains no clear explanation of why this has happened. I did referee a paper once for a journal to remain unnamed that proposed an explanation involving use of real estate by Japanese banks as collateral with the banks supposedly controlling their selling off of real estate in a way to make the market decline slowly as it did, but the paper was not accepted for publication and was never published anywhere to the best of my knowledge. In any case, the nature of what has gone on in that market remains a somewhat large mystery.

Seems like your point on India being more manufacturing intensive than Japan isn't really accurate

ReplyDeletehttp://data.worldbank.org/indicator/NV.IND.MANF.ZS?order=wbapi_data_value_2012+wbapi_data_value+wbapi_data_value-last&sort=desc

Ah, maybe not! My data source was different.

DeleteJapan is simply more and more inward looking. Foreign innovations and ideas are no longer studied or adopted. Japanese companies these days mainly focus on making products that appeal to Japanese domestic consumers, so its products seem less and less attractive to foreigners.

ReplyDeleteJapanese lifetime employment was always a myth. Fail to perform and you were shuffled off to a subsidiary, where you would be fired for continued failure to perform. (Although it would take longer than at a US company. And lifetime employment never covered more than 30% of the workforce.)

ReplyDeleteAlso, although I haven't looked at real estate prices recently, prices did recover significantly in the decade after the bubble bottomed out. Our little plot of land sits back from the street, accessed by a 2 meter by 15 meter lane. I thought about buying the 1 meter by 15 meter other lane on the other side of the concrete bunker that we live behind: the owner wanted four times what was reasonable for my pocket, and checking land prices, he was right. Fifteen square meters of Tokyo real estate was still worth more than a house in the US.

David,

DeleteIn most of Japan, real estate never bottomed out, although perhaps it has finally in the last year and started rising since Abenomics came in, quite possible, and about time. However, Tokyo, if that is where you are, is a special case. It bottomed out back around 2005-06, and has risen some since then, although that is also a matter of where you are in the world's most populous metro area. And part of the reason things remain high relative to US and many other places in most of Japan is precisely that the decline has been very slow, a few percent per year, which is what is so peculiar and unique about the Japanese real estate bubble, the slow decline after a much more rapid increase, again, the only noticeable bubble ever to behave that way according to the late Charles P. Kindleberger, who wrote _Manias, Panics, and Crashes_, the book the late Paul Samuelson said was the most important book anybody should read if they were going to engage in investing in asset markets.

"Tokyo, if that is where you are, is a special case."

DeleteYou are exactly right: Tokyo is where I'm at, and it is different. Pretty much the whole rest of Japan is a basket case. And that's not likely to change*. And it would have been 2007 or 2008 that I tried to buy that plot of land. (Greater Tokyo is something like 30% of Japan's population (and that's increasing even as Japan's population is beginning to fall), so it's not all that unrepresentative; give it a few more decades, and Tokyo's all that'll be left: sort of like the eggplant that ate Chicago in reverse.)

*: Speaking of change and Abenomics, I have a sneaking suspicion that Abe and the LDP would love to throw the agricultural lobby (i.e. rice) under the bus. If the courts force redistricting, the ag lobby won't be worth bothering with. And Japan, Inc. (i.e. Abe and the LDP) must be getting tired of the subsidies and having to fight for the 700% or so import tariff on rice every time there's a trade negotiation with the US.

Regarding the prevalence of fax rather than online office software (that was mentioned in the other site, I think in the comments), one reason might be that until very recently there were not really decent and standardized coverage of non-western alphabets. I believe that has changed in the last few years; but these things take time to percolate into big companies (another effect of having larger companies dominating)

ReplyDelete