At Bloomberg, I make the case that business cycle theory is just one of those areas where humanity has not yet been able to make much progress:

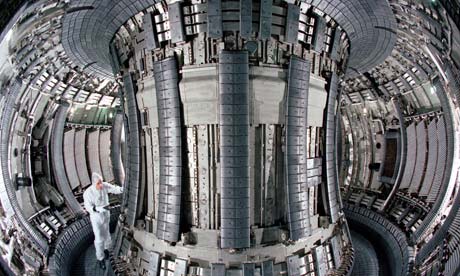

Fusion power, they say, is 30 years away…and always will be. Scientists figured out long ago that duplicating the power of the sun would provide us with almost limitless energy. But again and again, we’ve thrown our best brains at the problem and they’ve bounced off it like ping-pong balls.

Macroeconomics is a little like fusion power. When the Great Depression hit, economists finally started taking booms and busts seriously. There’s no denying that something weird happens when a country slips into recession -- all the same factories and offices and people and ideas are there, but suddenly people aren’t producing as much stuff. Why? John Maynard Keynes, Friedrich Hayek and Irving Fisher wrestled with this question in the 1930s, and their work kicked off a decades-long quest to understand what we now call the business cycle. But almost a century later, despite sending some of our best brains up against the problem, we’ve made frustratingly little progress.

It’s hard to overstate how few solid conclusions have emerged out of a century of macroeconomic research. We don’t even have a good grasp of what causes recessions...The stuff in the article will not be anything new to Noahpinion readers, but it brings a lot of different threads together. Read the whole thing here!

Here's a concept where recessions are like avalanches in a sand pile and the money supply is the sand ...

ReplyDeletehttp://informationtransfereconomics.blogspot.com/2014/03/the-monetary-base-as-sand-pile.html

I have a concept where recessions are like an outbreak of idiocy in blog comment threads, and the money supply is the spam.

DeleteI have a concept where recessions are like an outbreak of idiocy in blog comment threads, and the money supply is the spam.

DeleteROFL

To wit ...

DeleteI think this may be a little too strong. If the Fed wanted to produce a roaring inflation or crushing recession, I think they'd know how to do it. What is a real mystery is how to get just a teeny weeny bit more or less inflation or employment.

ReplyDeleteAnyone who doesn't know the difference between the monetary base and the money supply isn't ever going to understand inflation. Anyone who doesn't know the difference between the monetary base and the money supply should be writing economics pieces for Bloomberg.

ReplyDeleteI love the way Chicago school economists say that "no one" understands something, when what they mean is that Chicago school economists don't understand something.

ReplyDeleteExcept it's not a mystery, pretty much all US business cycles can be explained by good ol' sticky wages.

ReplyDeleteOf course, as we found out a bit ago, liberals like Noah don't actually trust the hoi polloi with dangerous knowledge, lest they do something their progressive overlords would not approve of.

So either Noah is yet again willingly obscuring the truth, or an economics education is worse than no education at all.

"Except it's not a mystery, pretty much all US business cycles can be explained by good ol' sticky wages."

DeleteYou might be able to create a completely unrealistic model in which sticky wages are the cause of 'business cycles' within that model, but that doesn't mean that sticky wages are the cause of business cycles in the real world.

You might be able to look at some actual data before spouting off uninformed comments.

DeleteBut the internet wouldn't be as fun then, would it ?

the data may show that wages are sticky, but that doesn't mean that sticky wages are the cause of business cycles.

DeleteThe data may show that water is wet, but that doesn't mean that too much water causes a flood.

DeleteOr some other nonsense.

you don't need to make completely unrealistic models to argue that too much water causes a flood.

DeleteThe unrealistic models I've seen are the ones that don't take stickiness into account.

DeleteUm, what about the overwhelming evidence that sticky wages are not nearly sticky enough to induce the effects NK models suggest?

DeleteI think sticky wages in the models are actually more than just sticky wages and the variable becomes a catch all for many different things. It is the NK version of TFP.

But scientists have known the mechanics of fusion for long time. little progress of been made about recession, market peaks, or other economic factors . So not an accurate comparison

ReplyDeleteThe analogy would work much better if macroeconomics has been stalled by lack of funding. ITER could have been built 20 years ago if it didn't require such a complicated international collaboration to put together all the money (and if the US fusion budget hadn't started declining since the 80s). With China and South Korea starting to pour serious money into fusion research (both of these countries now have world-class experiments and have grown impressive research programs out of scratch in a very short period of time) - I expect we will make much more progress on fusion energy than macroeconomics in the next 10-20 years.

ReplyDeleteAlso, despite the crippling lack of funding, there has been tremendous progress in fusion research in the past decades. But it's not the kind of progress that leads to sexy news headlines - mostly it is improvements in diagnostics and theory, and new experimental techniques (albeit applied on very old machines...).

ReplyDeleteThough, 1997 wasn't that long ago, when the Joint European Torus (which was built in the late 70's ahead of schedule and under budget) produced 16 million watts of fusion power over the course of a few seconds. JET is pretty old but it's still in operation, and in the next few years we will re-do the old 1997 experiments to aim for more fusion power produced than power put in (which looks very feasible - in fact, many people in the fusion community aren't that excited about it since it's such an incremental increase in performance from the '97 experiments) http://www.bbc.com/news/science-environment-27138087.

Sh*t happens!

ReplyDeleteA negative yieldcurve leads to recessions. Its a 100% predctor. Thus, we can avoid recession by keeping the yield curve positive.

ReplyDeletefalling GDP indicates recessions. Thus, we can avoid recessions by ensuring that GDP does not fall.

DeleteNot so. A falling GDP is not as good as a negative yieldcurve. Many times in the past this happens during a bull.

DeleteOk, and how do we keep the yield curve positive ?

Deletestop it from becoming negative, obviously.

DeleteAre you trying to fail the Turing test ?

DeleteWe can keep the yield curve positive by keeping the fed from raising rates

DeleteI long for the day when central bankers realise what a lousy instrument interest rate targeting is

DeleteI feel this piece wouldn't really serve a young person learning about macro for the first time. I would point them towards economic history and a history of economic thought.

ReplyDeleteWe don't have fusion power, but we have nuclear power and put a man on the moon.

Until recently recession were caused by the Fed which would raise rates to fight wage inflation. Lately we have had balance sheet recessions where debt and leverage levels get to much and asset bubbles pop. (and didn't the Fed allow the yield curve to go negative?)

Before we had price inflation because of rising wages. Now rising price inflation is caused by companies padding their profits.

Many Republican economists predicted (and still predict) runaway inflation because of the Fed's actions to help the recovery. They were wrong. Those who predicted that they were wrong were right.

The problem is that it is difficult to "prove" things in the social sciences and conclusions have political implications.

Such a fine example of reasoning from a price change.

DeleteMaybe you could spell your point out more clearly?

DeleteMy point is that you're engaging in fallacious reasoning.

DeleteIn what way? I said a bunch of different things. From your comment above about sticky wages you appear to have drunk the kool-aid and be highly ideological, that is your critical thinking skills aren't particularly well honed.

Delete"Of course, as we found out a bit ago, liberals like Noah don't actually trust the hoi polloi with dangerous knowledge, lest they do something their progressive overlords would not approve of."

Well okay then...

That's something Noah said himself a few weeks ago.

DeleteOf course, being the intellectually honest and brave soul he is, he deleted the comment and I didn't think of taking a screenshot at the time ...

Coming back to your comment

Until recently recession were caused by the Fed which would raise rates to fight wage inflation.

Apart from the Volcker-induced recession of the early 80s - which was indeed necessary to break inflation expectations - to what other recession does this story apply ?

balance sheet recessions

I hear this thrown around a lot on the internet. What it means, I'm not so sure.

asset bubbles pop

Since a "bubble" is something which can only be identified in retrospect, I find it's a useless concept. Someone who relies in his analysis on useless concepts is .... ? (I'll leave in the blanks for you to fill)

Before we had price inflation because of rising wages. Now rising price inflation is caused by companies padding their profits.

Last time I checked, inflation was caused by the money supply growing faster than output. Apparently, you've decided to go full obscurantist on the subject.

your critical thinking skills aren't particularly well honed.

If you want to know what the human face of Dunning-Krueger looks like, all you need to do is look in the mirror.

That's something Noah said himself a few weeks ago.

DeleteOf course, being the intellectually honest and brave soul he is, he deleted the comment and I didn't think of taking a screenshot at the time ...

???

Until recently recession were caused by the Fed which would raise rates to fight wage inflation.

DeleteYou do realize this is yet another confirmation of the sticky wages model, right ?

"Since a "bubble" is something which can only be identified in retrospect, I find it's a useless concept."

DeleteBecause as Bob Barker says, "The Price is Right!" And can be never be wrong! If it's wrong it will change and no longer be "wrong." Like when housing prices drop a third.

How would you describe what happened with the housing market? A price correction?

The money supply explanation might jibe with what I was saying. Before the excess money would go to wage earners and inflation would manifest itself in wage inflation. Now the excess money manifests itself in profit padding which boost prices as wage have been stagnant for a long time.

"You do realize this is yet another confirmation of the sticky wages model, right ?"

And yet you claim Volcker's recession was the only time this occurred?

I do think there is something to you ideas about the money supply and wage stickiness. I think higher inflation would make it easier to adjust.

However I would love to hear your theory about the recent financial crisis. There was no "housing bubble"? If we were able to cut many wage earner's pay to subsistence level there wouldn't been such a dramatic job loss in so short a period?

Your questions would be fully answered by opening a macro textbook.

DeleteBut, obviously, you can't be bothered to do that, you've got more important things to do - like spouting off uninformed opinions.

Fact 1 - financial markets are informationally efficient. It's called the EMH (I'm talking about the weak form). Therefore - BUBBLES DO NOT EXIST.

People who talk about bubbles are suffering from confirmation bias.

Fact 2 - the financial crisis was the result of a fall in nominal spending. WHICH IS EXACTLY WHAT THE STICKY WAGES MODEL PREDICTS.

So yet another point for good ol' sticky wages.

Fact 3 - internal devaluation is very unpleasant, and it takes a while. There's also the political dimension - deflation brings extremists to power.

The solution is reflation - that is, printing enough money to get everybody employed again.

My advice to you would be refrain from having strong opinions on subjects you do no grasp.

"Last time I checked, inflation was caused by the money supply growing faster than output"

Deleteyou're assuming constant 'velocity'.

Also, you ignore the possibility that price rises lead to an increase in the 'money supply', rather than the other way around.

DeleteIn my universe, rain isn't caused by puddles on the ground.

Deletewhat a silly analogy.

DeleteThere's a fine line between being open-minded and being stupid.

Deletethere's nothing stupid about the idea that the MV=PQ equation can be read from right to left, as well as from left to right.

DeleteNo response from you as yet regarding your assumption of constant velocity.

MV doesn't just rise without a reason. Saying that prices somehow raise MV is just dumb.

DeleteAnd no, I'm not assuming V is constant.

If things get more expensive for some reason, people have several options on how to react. One is to buy less, but another is to simply get more money elsewhere, by borrowing money or withdrawing from their savings. And if they do that, MV increases. Consumers have limited capability to borrow so that only tells part of the story, but it certainly seems like a factor.

DeleteOf course it occurs to me that a big simplification to what I just said is that in principle wages should tend to increase when P does, which dampens that tendency. Still, stickiness itself should tend to promote my argument since if wages are stickier than prices of goods that'll encourage people to find money elsewhere, and not all people make money from wages anyway.

DeleteSo the price level just rises for no reason ?

DeleteLike I said - idiots should refrain from having strong opinions on subject that are clearly beyond their graps.

Inflation doesn't just happen for no reason. My point was that if inflation happens, then that can cause MV to go up. It's also entirely the case that if M or V increases, that can cause inflation to go up. If the government just prints a bunch of money and people don't reduce the velocity at which they spend money, and the economy isn't able to grow to catch up, then inflation must then happen. But the causation goes both ways. It's not money then prices, and it's not prices then money, all four variables are moving around simultaneously and they each influence each other in different ways in order to maintain the accounting identity of MV = PQ.

DeleteInflation ultimately happens because of the aggregate result of individual people and organizations in the economy deciding to set prices. These actions are motivated by all sorts of psychological and economic factors. At the end of the day, P has to equal MV/Q, but M, V, and Q are themselves also influenced by many of the same psychological and economic factors, so "MV growing faster than Q" although technically true doesn't really tell you much.

DeleteSo the proper study of macroeconomists, therefore, is history.

ReplyDeleteMy view is that the answer lies in understanding effective demand... the primary concept of Keynes which has never been given a proper equation. I am researching a new equation that describes Keynes' view of effective demand...

ReplyDeleteEffective Demand >= Real GDP*effective labor share/(composite utilization of labor and capital)

Thus, effective labor share >= (composite utilization of labor and capital)

Effective labor share is determined by cycle limits of capacity utilization. For the US, effective labor share is 0.762*labor share index (non-farm business sector) since the 60's.

This equation has described the end of all business cycles since the 60's. We are right now again hitting the effective demand limit according to this equation. The limit could rise at this time extending the business cycle, which happened at the end of 90's and a bit before the crisis.

Very few are expecting the end of the business cycle now. The Fed and ECB are trying to keep the BC alive with long run low nominal rates. Will it work? Will the instability be too great? We will see.

In effect, there is an experiment going on right now with this equation of effective demand. If it turns out to identify the end of this business cycle, when few expect it, we will have made progress in understanding recessions. The equation can predict the potential end of a business cycle years in advance.

The equation is doing a great job so far in determining that potential GDP is much lower than the CBO originally thought.

Here is a synopsis.

http://effectivedemand.typepad.com/ed/synopsis-of-the-effective-demand-research.html

"The Fed and ECB are trying to keep the BC alive with long run low nominal rates. Will it work? Will the instability be too great? We will see."

DeleteYes we will. How will the instability manifest itself if it happens? Recession? Financial crisis?

My view is that Bernanke was too quick to pull back on QE. That raised mortgage costs and sucked demand out of the economy. My guess is that Yellen will delay raising rates unless the data shows the economy picking up speed. I think John Taylor is all wrong.

The economy is already picking up speed and has since 2013. Keeping rates low may not help it pick up any more speed if deleveraging is over and leveraging is happening.

DeleteEffective demand is as useful as the Easter Bunny or the man-friendly lesbian.

DeleteIt may be that the answers aren't so much economic as psychological.

ReplyDeleteSitting here on the sidelines, it sure appears to me that recessions are the name we give to those periods of negotiations between a large number of debtors and a large number of lenders regarding the payment terms on bad debt.

ReplyDeleteI'd be really interested to see a macroeconomic model starting in 2007 in which mortgage loans in (for example) Spain and the US could be quickly and easily written down.

I think it has something to do with the way risk (and the related perception of future rewards) propagates throughout an economy.

ReplyDelete[Man made] "Fusion power, they say, is 30 years away…and always will be."

ReplyDeleteNot true!!! Proof:

https://www.youtube.com/watch?v=qjnm3V0xYjI

If we don't know the causes of expansions and recessions, then we don't know that they (or at least some of them) are periodic, do we? To use the term 'business cycle' is to state a hypothesis; an alternate hypothesis is that the swings of the economy may not be cyclical at all.

ReplyDeleteOh dear, there has been discussion of some of this before. Yes, I agree that our understanding of macroecnomic fluctuations is not as good as we would like it to be, and indeed it looks like many recessions/depressions have their own unique peculiarities. Certainly this latest one was triggered by the collapse of the housing bubble and the related broader financial collapse.

ReplyDeleteSo, I would like to respectfully disagree with all those above loudly declaring that bubbles can only be identified in retrospect. False. There were many, starting with Dean Baker and including such people as Nouriel Roubini, and Robert Shiller, and, well, me, who called publicly that there was a housing bubble going on based on price to rent ratios being at historic highs and so on, with some of us, me again on the list, also calling that its collapse would lead to serious economic difficulties. That there was a group of economists, mostly non-mainstream, who called what happened pretty closely is a fact that has been discussed here previously. We should not have people saying the blatantly silly and false things I see being stated in this particular thread.

Even a broken clock is right twice a day.

DeleteIf you can't see that, then you're not as smart as you think you are. And you aren't.

Oh, and with your magical powers of forecasting, I'm guessing you went short on housing and made a fortune in the process.

DeleteWell, did you in fact make a fortune ? Or are you just monday morning quarterbacking ?

also calling that its collapse would lead to serious economic difficulties.

Seeing as how housing prices started declining in 2006 and the recession hit in late 2008, it would take a lot of squinting to see the connection.

Is this the best criticism you idiots have of sticky wages and EMH ?

Sorry, Daniel, but I was not one of those people who was sitting there for 8 years going "doom doom doom!" like Peter Schiff, who also was forecasting massive hyperinflation to come with the doom. In fact, over on Dean's blog, I just took him to task for claiming that nobody remembers the housing bubble and reminded him that while he and Roubini were forecasting in late 2006 that 2007 would be a year of recession because of declining construction that at that time I openly disagreed with them, accurately noting that depreciation of the dollar would bring a surge of exports, which it did, and which held the recession off for a good solid year.

DeleteHowever, in the summer of 2008 I warned that a full bore crash was coming very soon. The url does not seem to work directly, but Mark Thoma picked it up from Econospeak on July 12 of that year. You can find it by googling "gradual decline before the crash." The top hit gets you to Mark's discussion of my post and his link to it.

So, I do not want to get too pompous here, but I am in fact one of the very few people who really did call it pretty close to when it happened and was telling other people who were calling it too soon that they were doing so. Do a little checking before you come on like an ignorant jerk.

Barkley Rosser

The basic idea is that wages did not rise enough in the 05-07 timeframe as they should have, and the result was a financial crisis. People could not handle their debts in a large enough manner and the financial system got drained.

DeleteIf wages rise as they should have, nominal income fall is "typical" and we get a typical hard landing recession with unemployment peaking in the 8.0% range. No financial crisis, no seeing the ugly underbelly of finance.

I am in fact one of the very few people who really did call it pretty close to when it happened

DeleteLet me repeat myself - did you put your money where your mouth was ? Because hindisight is always 20-20.

Also, correlation does not imply causation. In fact, a financial crisis after a fall in nominal spending is exactly what the sticky wages model predicts.

So no, I'm not impressed by a model which totally fails to take into account the central bank's reaction.

The basic idea is that wages did not rise enough in the 05-07 timeframe as they should have, and the result was a financial crisis.

DeleteSo you're saying that money was tight ?

Gee, if I didn't know better, I'd say it's a point in favour of sticky wages.

Maybe we can start by not assuming that any one thing is responsible for causing either recessions or expansions.

ReplyDeleteBy far and away the best article on macroeconomics I have ever read. The only shocking thing about is that apparently it is so controversial.

ReplyDelete"The main statistical technique we have to analyze macro data -- time-series econometrics -- is notoriously inconclusive and unreliable, especially with so few data points."

ReplyDeleteNo time series analysis is NOT notoriously inconclusive and unreliable - it actually has many successes (like image processing or control theory). It just can't do miracles when availability of data is small AND data are observational AND NONstationary!